Comprehensive Guide to Residential Strata Insurance in NSW

Key Takeaways

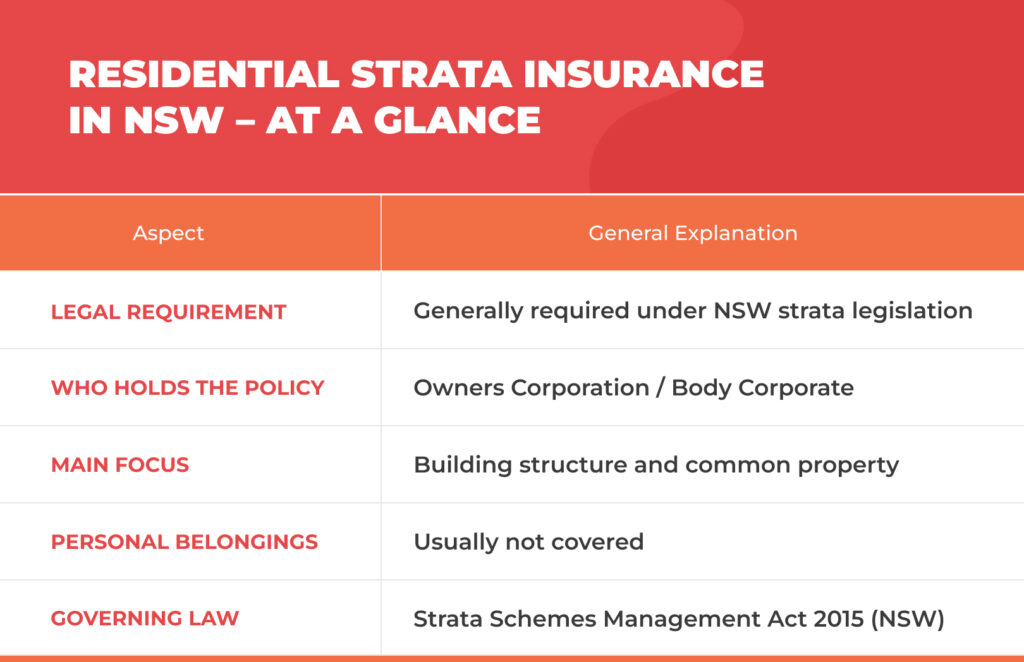

- Residential strata insurance NSW is in most cases a legal requirement for any strata-titled property as per NSW legislation.

- Normally, coverage is focused on communal facilities, common areas, and the building, with risks considered rather than individual contents.

- The policy features and optional covers may vary depending on the characteristics of the strata scheme and the specific insurer’s policy terms and conditions.

- In fact, a professional can help with documentation and compliance requirements within the scope of general information or services permitted under Australian law.

Residential strata living is one of the most popular features of the New South Wales lifestyle, particularly in apartment blocks, townhouses, and shared residential developments. Because more parties are involved, such as lot owners, committee members, and a strata manager, the insurance arrangements are usually more complex than those for a typical home. This guide explains residential strata insurance in NSW using straightforward, general, and law-friendly language so that readers can get a clear and accurate comprehension.

This information is general in nature and does not take into account your personal objectives, financial situation, or needs.

Understanding Residential Strata Insurance in New South Wales

Residential strata insurance covers shared risks arising out of strata titled properties. In NSW, such arrangements are regulated by law and are generally implemented by a strata company or body corporate, sometimes with assistance from a professional property manager.

What Is Strata Insurance?

Strata insurance is a policy that primarily covers strata title properties. It is usually mandated under the Strata Schemes Management Act 2015 (NSW). The insurance can cover the property's structure and amenities, such as common areas and conveniences available to all residents. Insurance generally does not cover the personal belongings of individuals living in the units, known as 'lots'.

Strata insurance is, in most cases, a separate insurance from the insurance an individual takes for their home, which generally covers the stuff inside the home.

Who Benefits From It?

Residential strata insurance is pretty much a common theme for:

- House owners residing in strata dwellings

- The body corporate who ensures that all obligations are met

- Strata managers are responsible for the daily administration

- The members of the committee and the office bearers who represent the scheme

Start your Quote today!

Key Features of Residential Strata Insurance

Having a clear idea of what is typically covered and what might be optional will definitely help you understand the structure of these policies.

Coverage Inclusions

Although the exact details differ depending on the provider and risk profile, residential strata insurance is generally concerned with:

- Home Building items and the physical building structure

- Common area contents, such as shared fixtures

- Storm, water, accidental, and malicious damages

Insurers typically do not cover problems caused by wear and tear, as these are generally considered maintenance issues.

Optional Covers and Extensions

Some optional covers that may be available under certain policies include:

- Machinery breakdown cover (e.g. lifts, shared pumps, or air-conditioning units)

- Catastrophe insurance for major insured events

- Pools and related infrastructure protection

The availability and scope of optional covers depend on the insurer, underwriting criteria, and policy terms and conditions.

Additional Benefits Commonly Considered

Residential strata insurance policies may also include, subject to the policy:

- Accommodation in case of necessity and Loss of rent after insured events

- Cover for volunteer workers helping the strata scheme

- Office Bearers liability and Legal Defence Expenses

- Property Damage Liability in the case of shared areas

In some cases, certain administrative or regulatory costs may be included, depending on the policy wording.

The Role of Strata Insurance Specialists

Many schemes engage a strata insurance specialist to provide support with understanding and administration, given the regulatory environment and diverse building designs.

Why an Insurance Broker Is Usually Involved

An insurance broker may assist by providing general information only, unless otherwise disclosed, including:

- Identifying the general advice boundaries

- Helping with insurance quotes and a Strata Insurance quote

- Ensuring Target Market Determination alignment

- Offering access to compliance tools and data insights

Before arranging any insurance, brokers generally provide a Financial Services Guide (FSG) and refer clients to the relevant Product Disclosure Statement (PDS), which should be reviewed carefully before making any decisions.

Industry Partnerships and Market Structure

Some brokers operate within broader industry networks. For example, VIM Cover is a member of the Steadfast Network, which is associated with the Steadfast Group Ltd, and may work with specialist underwriting agencies such as CHU Underwriting Agencies Pty Ltd.

This information is provided for general market awareness only and does not constitute a recommendation or endorsement of any specific broker, insurer, or underwriting agency.

Such agreements can facilitate a wider range of underwriting skills for strata properties in NSW and South Australia. Various entity codes may include ABN 18 001 580 and ABN 98 073 659 677, depending on the entity involved.

Steps to Secure the Best Strata Insurance Policy

Important Considerations for Strata Committees

Before reading the insurance policy or renewing it, a committee generally takes into account:

- The scheme’s total financial health

- Age of the building, type of construction, and communal facilities

- Claims record and risk profile changes

Sometimes, a committee member may coordinate with a strata manager to ensure that the documentation stays in line with the legislation and insurer requirements.

FAQs

Q1. Is residential strata insurance compulsory in NSW?

A1. Generally, the legislation requires that strata schemes in NSW maintain insurance for the building and the common property.

Q2. Does strata insurance replace home insurance?

A2. Strata insurance usually covers common/shared property, whereas home insurance covers items inside individual lots.

Q3. Are washing machines included in strata insurance?

A3. It appears that fixed infrastructure could be treated differently from appliances such as washing machines, which are usually considered personal property. Coverage depends on how items are defined in the policy wording.

Q4. Who is responsible for the strata scheme insurance?

A4. It is typical for the body corporate or strata manager to arrange this, and at times they may be assisted by an Insurance Broker acting within the scope of their authorised services.

Comprehensive Guide to Residential Strata Insurance in QLD

Key Takeaways

- Residential strata insurance in QLD is mainly about insulating common property and shared building elements in strata schemes.

- Insurance policies can offer different coverage, so it is a good idea to check the relevant Product Disclosure Statement and Target Market documents.

- Strata insurance is not simply a type of Home Insurance or Landlord Insurance; it differs in both its make-up and its aims.

- Industry participants may provide general information about types of general insurance without taking into account individual circumstances.

Residential strata insurance plays an established role in protecting and managing shared living environments throughout Queensland. Sometimes, even a small-unit complex or a multi-storey residential development can be a strata property. Besides multiple owners, it involves shared responsibilities, common risks, and key differences from single-family homes.

Understanding residential strata insurance in QLD helps strata owners understand the framework. It also explains the cover and exclusions.

This guide provides general information only. It is not financial product advice and does not take into account individual goals, financial situations, or needs.

Readers should refer to the relevant Product Disclosure Statement (PDS), Target Market Determination (TMD), and Financial Services Guide (FSG) before choosing an insurance product. They should also seek independent professional advice if necessary.

What Is Residential Strata Insurance?

A Body Corporate usually organises residential strata insurance for strata-titled properties such as apartments, duplexes, and townhouses. Instead of a single dwelling, this insurance usually covers the strata building, common areas, and shared facilities. These facilities are used by multiple occupants.

Residential strata insurance in Queensland generally refers to insurance for strata properties regulated under the Body Corporate and Community Management Act. This act sets out the insurance requirements for strata schemes. Even though coverage varies, policies are usually for the property insured, not for the personal belongings of individual lot owners.

Start your Quote today!

Understanding Strata Insurance Basics

A key characteristic of residential strata insurance QLD is that it generally insures common property and areas. Examples include hallways, lifts, stairwells, gardens, driveways, and shared amenities such as swimming pools. The idea is to protect collectively owned and maintained places, even though individuals do not privately hold them.

Depending on the policy wording, strata insurance may cover insured events such as accidental damage, storm damage, and water damage. The extent of cover is determined by the inclusions and exclusions listed in the policy documents.

In fact, most strata insurance policies include a public liability section that covers injuries or property damage in common areas. Consequently, this kind of cover is especially necessary when visitors, residents, or even volunteers use shared facilities.

Why Residential Strata Insurance Is Relevant for Strata Title Properties

Queensland legislation imposes a general obligation on bodies corporate to ensure appropriate insurance is in place for their strata schemes. This insurance mandate reflects the co-ownership aspect of strata buildings and the consequent need to manage risk collectively in Australian strata settings.

Typically, residential strata insurance covers the risks of the physical building, including permanent fixtures and contents in common areas. In contrast, it differs from the content insurance policy arrangements held by individual lot owners.

Although strata insurance applies to communal property, individual lot owners may hold separate Home Insurance or Landlord Insurance policies. These policies can cover personal contents, floating floors, or alterations not classified as common property under strata legislation and scheme by-laws.

Key Inclusions Commonly Found in a Strata Insurance Policy

Coverage for Strata Properties

Typical inclusions might generally be:

- The physical structure of the building and the specified building sum

- Contents in the common area, like lights, fixtures, or communal equipment

- Rent loss due to an insured event that disrupts tenancy arrangements

Additionally, certain insurance policies can highlight Office Bearers' cover or safeguards. This protects committee members when they perform their official duties.

Additional Coverage Areas

Optional sections may concern the following, depending on the insurance products:

- A machinery breakdown that affects the shared systems

- Property damage cover is limited to the involvement of shared facilities

- Clearly defined liability issues relating to voluntary workers

The availability of coverage depends on the policy terms and the insurer's Target Market.

How Insurance Premiums Are Commonly Influenced

Factors Influencing Insurance Premiums

One factor alone is rarely the reason behind the increase or decrease of insurance premiums for residential strata in QLD. The insurance company may consider the claims made on the strata property over the last few years, the strata's risk profile, and the value of your home as part of the whole building.

Moreover, factors such as points of cover, previous loss events, claims history, and building characteristics may also be assessed. For this reason, premium rates differ between insurers and policy types.

Reading the Product Disclosure Statement

The relevant PDS would cover what is included and excluded, the limits, and the claims procedure. Going over this piece helps the parties involved clarify the definition of the cover and when it applies.

On the other hand, the Financial Services Guide and the like clarify the delivery of insurance services and the role of intermediaries. Collectively, such documents constitute the wider disclosure framework under Australian financial services law.

Strata Management and Insurance Responsibilities

Role of Strata Managers and Committees

Strata management is a system usually composed of a strata manager, the strata committee, and the owners of individual lots. They share several responsibilities, including ensuring the body corporate has insurance, complying with strata scheme regulations, and handling collective decision-making processes.

In most cases, good strata management is a matter of committee members and residents talking regularly about insurance options, claims, and any changes introduced by a new policy.

Secure Your Strata Property with the Right Insurance

This guide focuses on Queensland. However, residential strata insurance frameworks in New South Wales and South Australia may differ due to variations in legislation and regulations.

The specific needs and characteristics of local areas, building types, and the use of strata-titled properties influence insurance arrangements.

This content does not constitute financial product advice and does not take into account individual objectives, financial situations, or needs.

FAQs

Q1. Is residential strata insurance the same as a Home Insurance policy?

A1. No. A Home Insurance policy usually covers a single dwelling, while strata insurance generally covers shared building elements.

Q2. Does strata insurance cover personal items?

A2. Personal items and belongings are typically covered under individual contents insurance, not strata insurance.

Q3. Who arranges residential strata insurance in QLD?

A3. The Body Corporate generally arranges it on behalf of the strata schemes.

Q4. Are all events automatically covered?

A4. Coverage depends on policy terms, insured events, and exclusions outlined in the Product Disclosure Statement.

Understanding Insurance for Service Businesses

Why Understanding Insurance Matters for Service Based Businesses

Whether you offer consulting, accounting, hairdressing, graphic design, IT support, or any kind of professional service, insurance forms a critical part of your business’s stability. Clients rely on your expertise, and you depend on a world of trust and relationships — but what protects you when things don’t go as planned? The answer is comprehensive, fit-for-purpose insurance.

Service businesses face unique risks. A wrong recommendation, unintended copyright infringement, or client dissatisfaction can quickly spiral into expensive legal battles. Even something as simple as a client slipping on your premises can threaten hard-earned revenue. An unexpected incident may disrupt your ability to deliver services altogether. Insurance helps you manage these uncertainties so you can focus on growing your reputation and serving your clientele without unnecessary worry.

Why service-based businesses need insurance

Professional agility is one thing; professional security is another entirely. No matter how skilled or careful, every services business is exposed to risk. It’s easy to assume that “insurance” is just for brick-and-mortar businesses who deal with inventory or physical products, but that view can leave service providers dangerously exposed.

A dissatisfied client could allege professional negligence. Sensitive client data could be hacked, resulting in a privacy breach. Someone could visit your office, trip on a loose carpet, and be injured. Without insurance, each of these examples could cause disruption, loss of income, and even legal liability that threatens your livelihood.

Consider these common misperceptions:

- “We just give advice, there’s nothing that can physically go wrong.”

- “My client base is loyal, I don’t expect them to sue.”

- “I work from home, so risk is minimal.”

Unfortunately, court cases and complaints don’t distinguish between intentions and outcomes. A single client misunderstanding, system hack, or oversight can bring intense financial stress. Insurance is about safeguarding your business so you can deliver professional services confidently.

Key types of insurance for service-based businesses

Just as no two service businesses are identical, insurance solutions aren’t one-size-fits-all. Here’s a rundown of the main types you should consider:

Professional indemnity insurance

This is the cornerstone for most consultants, advisors, and professionals. It protects you if a client alleges that your advice or service caused them financial loss, either through error, omission, or negligence.

Common claims covered:

- Advice deemed erroneous that leads to a client’s monetary loss

- Accidental breach of copyright or confidentiality

- Defamation related to your services

- Loss of client documents entrusted to you

Some industries require professional indemnity insurance by law or regulation — such as accountants, lawyers, financial advisors, and some allied health practitioners.

Public liability insurance

This covers third-party injury or property damage that occurs as a result of your business activities. For instance, a client might slip and hurt themselves at your workplace, or you accidentally damage something while visiting a client.

While public liability may seem like “retail business” cover, it’s vital for service businesses who engage with clients in person — even if only occasionally.

Cyber liability insurance

Service businesses often hold sensitive client data. Cyber liability deals with the risks of hacking, cyber-theft, or accidental release of private information.

Covers events like:

- Data breaches involving client records

- Ransomware and email scams

- Losses from unauthorised electronic fund transfers

General business insurance won’t typically cover cyber-related incidents, making this increasingly essential.

Business interruption insurance

Events beyond your control — like storm damage, fire, or theft — can prevent you from servicing clients, sometimes for weeks or months. Business interruption covers loss of income so your business survives while you get back on your feet.

Management liability insurance

This is relevant once your service business expands or you run a company structure with directors. It protects personal and company assets in the case of management-related claims, workplace disputes, or regulatory penalties.

Portable equipment insurance

Service professionals sometimes work with valuable tech, tools, or equipment outside the office — think laptops, cameras, or medical devices. Portable equipment cover insures these against loss, theft, or damage.

Typical insurance needs by service sector

Insurance priorities vary by profession, but some overlaps are universal. Here’s a simplified table to illustrate typical needs:

| Service Sector | Professional Indemnity | Public Liability | Cyber Liability | Business Interruption | Equipment Cover |

|---|---|---|---|---|---|

| Accounting/Finance | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Legal | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| IT/Tech Support | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Creative/Design/Media | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Health & Wellness | ✔️ | ✔️ | ✖️ | ✔️ | ✔️ |

| Consultancy/Advisory | ✔️ | ✔️ | ✔️ | ✔️ | ✔️ |

| Trades (Service-only) | ✔️ | ✔️ | ✖️ | ✔️ | ✔️ |

Not every business needs every type, but this provides a starting point for considering where your business faces greatest exposure.

Assessing your risks

Assessing which insurance you need starts with a careful look at your activities and obligations. No two businesses face identical risks, but common questions help clarify your unique profile:

- Who are my clients, and what promises do I make to them?

- Do I handle confidential information or client data?

- Do I work at client sites or welcome visitors?

- What technology or specialised equipment do I rely on?

- What would happen if my premises were inaccessible for a week?

- Am I exposed to claims about my work quality, accuracy, or conduct?

- Are there regulatory requirements or client contract terms mandating specific covers?

By mapping out the services you provide and the way you interact with clients, you paint a clear picture of where you may be vulnerable. It also helps avoid paying for unnecessary cover.

How much insurance cover is enough?

Under-insuring is risky, but over-insuring ties up capital unnecessarily. Finding the right balance requires thinking beyond headline policy limits. Some key factors include:

- The size and complexity of your contracts

- Industry standards or legal minimums

- Value of equipment and assets

- Potential legal defence and settlement costs

- Duration your business could survive a disruption without income

Ideally, insurance should be tailored. Discussing your specific risk factors with a broker or insurance adviser can help fine-tune levels, especially where clients or government expect set minimums.

Common pitfalls and how to avoid them

Insurance for service providers has plenty of nuances. Some common mistakes trip up even experienced operators:

- Ignoring contract terms: Many larger clients or government contracts specify insurance types and limits. Overlooking these can cost you contracts or expose you to claims.

- Assuming home-based businesses don’t need cover: Running a service business from your home doesn’t exempt you from risks — and most personal insurance policies exclude commercial use.

- Not updating insurance as the business grows: Expansion, new services, or hiring staff all change your risk profile. Annual reviews ensure your cover keeps pace.

- Failing to disclose full activities to insurers: Not telling your insurer exactly what you do (all the services you offer, where you operate, etc.) can void policies if you ever claim.

The relationship between risk management and insurance

Insurance is your financial backup; risk management is what prevents claims in the first place. They work hand in hand.

Service business owners should embed simple practices to reduce common exposures. These include:

- Clear, written client agreements spelling out what you’re responsible for

- Maintaining professional credentials and keeping skills sharp

- Regular technology and cybersecurity updates

- Confidentiality and document management protocols

- Procedures for safely greeting clients and visitors

Implementing practical controls can limit the likelihood of incidents and support your case if you do need to claim.

Adapting your cover as things change

Your business rarely stands still. Insurance needs shift as you:

- Diversify your services

- Hire more staff or contractors

- Invest in new technology

- Land bigger clients or contracts

- Move offices or go fully remote

Annual insurance checkups should become routine, just like tax or compliance reviews. These keep your cover fit for purpose so you’re not caught short if things go sideways.

Working with insurance advisers and brokers

Navigating insurance products and wordings can feel like a maze. For many service businesses, building a relationship with a broker or adviser is money well spent.

Brokers help identify gaps, explain policy conditions, and negotiate on your behalf — especially valuable if need to claim. Their insights into industry-specific risks are drawn from real-world experience, helping you avoid the most common (and costly) pitfalls.

Don’t be afraid to ask direct questions about exclusions, waiting periods, or policy conditions. A trustworthy adviser expects it. Their goal is to help your business thrive, not just sell insurance.

Key takeaways for service business owners

Being a service professional means people trust your knowledge, integrity, and expertise. The right insurance lets you back that up, with confidence. Always be proactive: review your exposure, tailor your policies, communicate openly with your broker or insurer, and update cover as you grow.

At its heart, insurance for service businesses is about more than ticking a compliance box. It provides the resilience you need to keep doing what you do best, even if the unexpected happens. As your business grows, make insurance part of your strategic toolkit — not just an afterthought.

Manufacturing and Engineering Insurance

Manufacturing and Engineering Insurance: Risk Management Essentials

Australian manufacturers and engineering firms operate in a world where progress and risk walk side by side. Machinery hums, innovation thrives, but so do hazards: equipment failures, supply interruptions, cyber threats, and complex liabilities. No matter how robust your systems or safety protocols, unexpected events can derail even the most seasoned operations.

Protecting the heart of your business isn’t just about ticking a regulatory box; it’s a strategic investment in continuity and resilience.

Why Traditional Insurance Falls Short

General insurance policies simply don’t cut it when it comes to the intricate world of manufacturing and engineering. These sectors face an interplay of physical, human, and digital risks that are often unique. Many insurance products were not designed with an advanced CNC facility or a 3D-printed medical device manufacturer in mind.

From precision tooling to global supply chains, the risks are multifaceted:

- Production lines can grind to a halt from mechanical or software failures.

- Intellectual property could be compromised during a cyber intrusion.

- An error in a single engineered component may affect hundreds of downstream users.

- Environmental and pollution incidents could trigger regulatory fines and third-party claims.

So, what does a tailored manufacturing and engineering insurance policy actually cover?

Core Components of a Robust Policy

At the foundation, specialist insurers target both tangible and intangible threats, making these products more sophisticated than standard business packages. Typical covers might include:

| Coverage Type | What It Protects | Why It Matters |

|---|---|---|

| Machinery Breakdown | Physical assets and income loss | Machines are business lifeblood |

| Product Liability | Legal costs, damages | Defective products can result in recalls |

| Business Interruption | Lost income, extra costs | Downtime has a cascading financial effect |

| Professional Indemnity | Errors in design, advice, or plans | Even the best engineers make mistakes |

| Cyber Liability | Data and networks | Attacks can halt operations instantly |

| Environmental Impairment Liability | Pollution events | Manufacturing accidents can be costly |

| Transit and Marine Cargo | Goods in transit | Supply chains often cross national borders |

| Property Damage | Buildings, contents, stock | Fires and weather events threaten assets |

This combination adapts as your business grows, automates, or integrates new technology.

Digging Deeper: Customised Protections

No two facilities or product lines look exactly alike. Insurance programs need to account for the nuance of your machinery, materials, and markets. For example:

- An electronics manufacturer may face acute risks around static discharge and temperature control. Their insurance should include specific endorsements for equipment breakdown and data restoration.

- A precision engineering firm providing components for automotive assembly lines must look at recall cover, protecting against the cost of pulling back defective products across a continent.

- Multi-site operators might require blanket coverage that flexes as stock is moved between locations in Australia or overseas.

These tailored policies are engineered not just to pay claims, but to help companies bounce back swiftly after a disruption.

The Modern Threatscape: Beyond Tangible Loss

Digitalisation reshapes the sector, and with it, fresh challenges. Australian engineering and manufacturing firms now face:

- Sophisticated ransomware attacks that lock down plant control systems.

- Intellectual property risk as design files are shared with global partners.

- Breach of contract disputes arising from software glitches in high-stakes projects.

Insurance now reaches beyond the warehouse floor to digital blueprints, data integrity, and global supply contracts. The sharp increase in cyber events, for instance, makes cyber liability cover non-negotiable for even mid-sized firms.

Case Study: When the Unexpected Happens

Picture a mid-sized manufacturer near Geelong. A power surge damages their main CNC lathe, leading to a three-week halt in production. While repairs are underway, pending orders pile up, overtime rises, and clients express their frustration.

If their insurance is narrowly focused, machinery repair costs may be covered, but the lost income, expedited shipping costs to placate angry clients, and penalty payments may fall outside the policy.

Comprehensive business interruption cover, however, transforms the outcome:

- Lost gross profit during downtime is covered.

- Extra expenses incurred to keep customers happy can be claimed.

- The business sustains its reputation and retains valuable contracts.

Commonly Overlooked Exposures

Many businesses think only in terms of fire, theft, and machinery breakdown. Yet experience shows the less visible risks can be even more damaging:

- A minor production error in an aluminium extrusion triggers a large-scale product recall.

- Environmental exposures from leaks or mistimed waste disposal prompt regulatory scrutiny.

- Contractual disputes arise when finished goods are late due to material shortages.

These scenarios underscore the need to periodically review your policy for exclusions and sub-limits, to avoid an underinsurance trap.

Emerging Coverage Trends for Australian Manufacturers

New legislative frameworks and technology adoption trends continue to reshape the insurance landscape:

- ESG (Environmental, Social & Governance) standards have led to stricter environmental liability requirements.

- The adoption of Industry 4.0 automation calls for breakdown covers that extend to robotics and IoT-integrated systems.

- Supply chain risk management tools are bundled with insurance, giving early warning of a brewing crisis overseas.

- Multinational operations are using master policies with local compliance overlays, harmonising coverage across multiple jurisdictions.

Insurance brokers working exclusively in the manufacturing and engineering sectors now harness data analytics, site risk mapping, and incident simulation tools to build adaptable policies. This arms decision-makers with the insights required to balance risk appetite with cost.

Cost-Saving Strategies Without Cutting Corners

Premiums for these advanced covers can be eye-watering, but there are effective ways to control costs without leaving yourself exposed:

- Invest in preventative maintenance and safety training, which can lower premiums through demonstrable risk reduction.

- Bundle multiple insurance types with one specialist provider for multibuy discounts and coverage clarity.

- Raise deductibles where appropriate, as long as you maintain sufficient liquidity to cover an initial loss.

- Engage periodically with your insurer to update them on equipment upgrades or process improvements—they may view you more favourably at renewal time.

A broker who understands both your business and your sector’s global risk profile is more likely to negotiate the right coverage at a fair rate.

Navigating Claims: How to Prepare Ahead

The difference between a smooth recovery and a drawn-out saga often lies in preparation. Forward-thinking firms:

- Keep digital and hard copies of critical documents such as invoices, maintenance logs, and certifications.

- Map key supply chain dependencies, so that loss adjusters understand business impact.

- Train key staff on claims notification protocols, ensuring all relevant evidence is collected promptly after an incident.

A little groundwork upfront can transform a frustrating experience into a quick and constructive claims resolution.

Top Mistakes to Watch Out For

Even sophisticated manufacturers sometimes get it wrong. Some of the most common pitfalls to avoid include:

- Assuming “one size fits all” business insurance policies are adequate.

- Failing to update policies after process changes or equipment upgrades.

- Overlooking cyber and environmental exposures.

- Ignoring contractual liability extensions demanded by clients or contractors.

Bringing an expert into your corner can provide crucial insight, often uncovering gaps that aren’t visible until a loss occurs.

Questions Business Owners Should Be Asking Themselves

Insurance is never a “set and forget” topic. It’s worthwhile to regularly challenge assumptions with questions like:

- Is my business interruption sum insured based on outdated financials?

- Have we accounted for all locations and their unique risks?

- If a new client requests a higher liability limit, can our current policy flex to meet it?

- Do our IT security protocols satisfy the terms for cyber insurance?

- Are there upcoming regulatory changes in the industries we supply that could leave us exposed?

Periodic reviews, particularly with specialist guidance, can make all the difference.

Industry Insights and Shaping the Future

Australian manufacturers are globalising, automating, and morphing into more data-driven businesses by the year. This modernisation has seen the insurance market respond with new products that reward proactive risk management and fast adaptation.

Firms embedding environmental sustainability, integrated IT controls, and world-class safety regimes are set to benefit with more attractive premiums and higher policy limits. Likewise, those that see insurance as a strategic partner rather than a cost find themselves better positioned to win complex tenders and attract global customers.

Success isn’t just about making things. It’s about safeguarding your ability to keep making, innovating, and delivering—even in the face of uncertainty.

As the future of manufacturing and engineering in Australia grows more complex, so too does the toolkit for managing risk. Structured well, specialist insurance is less an overhead, more the foundation on which sustainable success is built.

Why Hospitality Insurance is Crucial for Your Aussie Business

Why Hospitality Insurance is Crucial for Your Aussie Business

Running a restaurant, café, bar, boutique hotel or even a food truck is as much about crafting memorable experiences as it is about hard work, risk-taking and dealing with the unexpected. Hospitality, more than most industries, feels the pressure from every angle: environmental events, customer expectations, reputational risks, health and safety concerns, and the unpredictable rhythm of seasons. Even the most seasoned professionals have found themselves facing setbacks that came out of nowhere.

Risk management is woven throughout every shift, menu change and event, but some risks are too unpredictable or costly to plan for with process alone. This reality is what makes hospitality insurance not just a safety net but a core part of every serious business plan. Regardless of size or niche, being properly insured can mean the difference between weathering a major challenge or shutting your doors for good.

Understanding the Landscape — What Makes Hospitality Unique

The very nature of hospitality is personal. You’re often dealing with the public directly, people from all walks of life, and sometimes in high volumes or fast-paced environments. Safety, compliance and great service run side by side, but the list of things that can go wrong is extensive:

- A customer slips and sustains an injury on your premises

- Food served results in an allergic reaction

- Unexpected equipment failure spoils thousands of dollars’ worth of stock

- Storm damage, fire, or water leaks force an abrupt closure

- Staff injure themselves at work

- A serious data breach exposes sensitive payment details

These scenarios don’t just result in lost income; they trigger legal challenges, reputational damage, and existential questions. This is why insurance for hospitality businesses stands apart from general business cover.

The Core Types of Hospitality Insurance

Choosing the right cover isn’t always straightforward, as the industry requires several policies working together to fill the unique risk profile each business faces. The most typical policies are:

|

Insurance Type |

What it Covers |

Who Needs It |

|---|---|---|

|

Injury or property damage to others |

All businesses open to public |

|

|

Product Liability |

Issues arising from food or drinks served |

Food & beverage establishments |

|

Property Insurance |

Damage or loss to building and contents |

Bars, cafés, restaurants, hotels |

|

Loss of income due to closure from covered events |

All hospitality businesses |

|

|

Workers’ Compensation |

Employee injuries or illness at work |

Any business with staff |

|

Legal fees for management-related claims |

Companies, partnerships |

|

|

Data breaches, hacking, digital risks |

Handling online bookings/payments |

|

|

Equipment Breakdown |

Malfunction of key equipment (fridges, ovens, etc) |

Any reliant on machinery |

Every operation has different needs, and the best cover is always tailored to the activity, size and location involved.

Real-World Losses: Why General Business Insurance Isn't Enough

Hospitality businesses face exposures that aren’t typical for other trades. General policies are often silent on things like alcohol service, live entertainment, food contamination or large group functions. That’s why hospitality-specific wording makes insurance work in the real world.

For example:

- A specialty coffee shop in Melbourne lost its entire roasted coffee stock and several fridges to a major power outage caused by street works next door. General property cover replaced the hardware, but a tailored business interruption add-on helped the owners cope with additional expenses and loss of income during their busiest time of year.

- A boutique hotel on the Gold Coast faced a costly legal claim after a guest suffered an allergic reaction, even with allergens clearly marked. Without product liability included in their policy, substantial legal and medical bills threatened the business’s future.

Tailoring Protection to Your Venue

No two hospitality ventures carry the same risk, and reviewing insurance should be as regular as reviewing menus or pricing. Here are some variables that influence your best combination of covers:

- Do you run events, entertainment, or have outdoor seating?

- Is alcohol part of your offering?

- Are you predominantly cashless or reliant on digital technology?

- Do you offer food delivery, or partner with third-party apps?

- How many staff do you employ? Are they full time, part time, or casual?

- Are you part of a franchise or independent operator?

- What is your premises’ location — high traffic, coastal, city centre, or rural?

An experienced insurance advisor familiar with the hospitality trade will use these answers to recommend specifics regarding risk limits, extensions, and exclusions.

Common Gaps and Overlooked Risks

Some hazards are frequently missed until a business faces a claim. Time and again, operators wish they’d looked closer at these:

- Flood Damage: Plenty of general property policies exclude or heavily limit flood cover, even in areas not traditionally flood-prone. Given Australia’s weather unpredictability, consider a dedicated flood endorsement.

- Wine, Spirits, and Perishables: Premium inventory, like aged wines or rare ingredients, are often underinsured. Specific declarations protect rare or irreplaceable stock.

- Emerging Cyber Risks: Online bookings, digital gift cards and cashless transactions expose venues to identity theft, fraud, and ransomware. A cyber policy not only helps with recovery but also includes costs around customer notifications and even brand repair.

- Temporary & Agency Staff: Many venues operate with a casual workforce; some workers' compensation and liability policies do not cover agency staff unless specifically added.

- Reputational Harm: Social media storms or a single food safety incident can cost more than property loss. Some insurers offer coverage for response and PR management as part of crisis protection, which is worth discussing for venues with big public profiles.

Hospitality Insurance in Action — How Claims Work

Dealing with a crisis is always stressful, but having a clear, proactive relationship with your insurer or broker helps turn the process into something far more manageable. Effective claims processes may include:

- 24/7 emergency phones for major incidents

- Assistance with suppliers and repairers on short notice

- Dedicated claims contacts who understand hospitality

- Advance payments on larger claims to preserve cash flow

- Guidance with regulatory authorities and customer communications

A busy café that suffered arson over a long weekend might use insurance to clean up quickly, fund temporary relocation of catering orders, and cover ongoing staff wages – all before full damage assessment is even complete. This flexibility gives business owners very real peace of mind and lets them focus on recovery.

Making Your Insurance Work: Tips for Owners and Managers

Insurance is more than paperwork and payments. Getting real value means actively managing risk, and working with your provider, not just paying them. Here’s how to build the strongest safety net:

- Review your cover annually, especially before renewals

- Update sums insured to reflect real replacement values

- Maintain detailed documentation of assets, receipts, maintenance schedules

- Take extra care over staff training in food handling, alcohol service, and customer safety

- Report changes (like renovations, changes of business activity, adding delivery) to your broker as soon as they happen

- Understand the process for minor vs major claims, and ensure your team knows who to call

A table of more tips:

|

Action Point |

Why it Matters |

|---|---|

|

Update stocklists regularly |

Claims are faster and more accurate |

|

Keep digital backups (off-site) |

Essential for fire, theft, flood recovery |

|

Develop a crisis communication plan |

Protects your reputation and calms customers |

|

Involve staff in risk awareness |

Fewer accidents, better claims outcomes |

|

Evaluate policy excesses |

Matches your cash flow and claim history |

Looking Forward: The Future of Insurance for Hospitality

Insurers who understand hospitality are constantly evolving products to respond to modern realities. As climate, technology and consumer trends shift, so too do the types of cover becoming most valuable:

- Climate risks prompt more flexible business interruption solutions

- Technology offers usage-based policies, lowering costs when venues are closed or on quiet periods

- Increasingly flexible liability solutions for venues hosting pop-ups, markets or incorporating off-site catering

- Greater focus on data privacy and cyber breaches

Australian hospitality is famously resilient and creative. Backing that spirit with smart insurance means not just surviving disruption, but standing confidently when the next challenge comes knocking. It’s about giving owners, managers, and staff the security to focus on what’s really important: looking after guests, building brands, and creating the moments that keep customers coming back.

Why Property Managers Need a Diligent Insurance Broker

Why Property Managers Need a Diligent Insurance Broker in 2025

The Evolving Role of Insurance Brokers in Real Estate.

It’s one thing to keep real estate humming along smoothly; it’s another to ensure every asset, every client, and every transaction is protected beyond the bare minimum. Property management demands multitasking, adaptability, and a clear head amid chaos. But even the sharpest operators occasionally face setbacks they never saw coming: an unexpected fire, a disgruntled tenant alleging negligence, or a major storm that leaves half a complex uninhabitable.

A robust insurance policy can soften the blow—if it actually covers what you need, with no shocking exclusions or loopholes lurking in the fine print. This is why having a genuinely diligent insurance broker isn’t just nice to have. It’s essential.

Why Property Managers Can't Afford Guesswork with Insurance

Property managers wear many hats: negotiators, mediators, maintenance coordinators, financial planners, and sometimes, crisis managers. Navigating insurance on your own, with its labyrinth of jargon, ever-shifting requirements, and fine-lined technicalities, can sap precious time and energy.

A diligent broker lifts that load by:

- Interrogating every nuance of your risk profile

- Tracking changes in local laws, rent defaults, tenant damage exclusions, and more

- Advocating strongly for you at claim time, rather than fading into the background

It’s tempting to rely on off-the-shelf insurance covers because they’re quick. But when disaster strikes, cookie-cutter solutions rarely fit the specific demands of managing tenancies, maintenance liability, or commercial strata.

The Subtle Traps in Property-Related Insurance

Insurance policies can look neat and comprehensive at a glance. Buried inside, though, are exclusions and ambiguous clauses that could undermine your resilience in a crisis.

Some common property management pitfalls include:

- Underinsurance: If a building is undervalued, payouts may be capped far below the true cost of repair or rebuild.

- Incorrect policy types: Residential and commercial risks are distinct; a policy written for one often short-changes the other.

- Ambiguous liability clauses: These might leave property managers personally exposed for tenant injuries or defects.

- Rent default loopholes: Not all policies treat loss of rent equally, especially in cases of tenant hardship or government intervention.

If you’re responsible for a block of apartments, holiday lets, mixed-use complexes or even single dwellings, aligning specific risks with appropriate technical cover is where a true broker excels.

What Sets a Diligent Insurance Broker Apart?

Not every insurance intermediary performs at the same level. The real standouts are meticulous, inquisitive, and communicative; they get genuinely invested in the ongoing security of your business.

Here’s what to look for:

1. Proactivity A diligent broker doesn’t wait for you to submit a policy renewal request. They monitor legislative updates, local risks, and emerging threats so policies are always current.

2. Risk Assessment They scrutinise the unique details of each property or portfolio and recommend cover specific to your needs, not just the insurer’s interests.

3. Transparency No glossing over exclusions or ambiguous fine print: you’ll get clear explanations of what’s covered, what’s not, and where you may be vulnerable.

4. Claims Advocacy When claims arise, proactive brokers handle negotiations, push back on unfair denials, and secure swift payouts. They’re accountable when it matters most.

5. Education They keep you in the loop about best practices in risk management, new product developments and market trends that may benefit you.

This isn’t just about selling policies, but forming a strategic partnership.

The Value of Customised Cover

Generic solutions leave you exposed to losses that could have been anticipated and insured against. A focused broker tailors protections for all angles of risk.

Consider the spectrum of exposures:

| Risk Type | Example Scenario | Specific Cover Required |

|---|---|---|

| Fire & Catastrophe | Blaze destroys common areas | Building and contents insurance |

| Tenant Negligence | Accidental flooding from overfilled bath | Tenant damage extension |

| Owner's Corporation | Dispute on maintenance responsibility | Strata liability |

| Rent Default | Sudden tenant bankruptcy | Loss of rent or rent default |

| Legal Liability | Slip-and-fall on wet tiles | Public liability |

| Valuation Errors | Asset rebuild cost underestimated | Full-sum insured recalibration |

Each field in that table is a live risk to your reputation, finances, and sometimes, personal standing. A diligent broker regularly reviews and updates all forms of cover in collaboration with you.

Claims Time: Where Diligence Makes the Difference

A properly handled claim is often the litmus test of a broker’s value. While some may step back after a sale, the best advocates step up, managing both communication and process, and helping avoid technical disputes that can delay or reduce settlements.

A diligent broker:

- Files paperwork quickly and accurately

- Gathers necessary evidence on your behalf, including valuations, photos or inspection reports

- Negotiates with insurers to avoid underpayment or unfair rejection

- Keeps you updated and reduces unnecessary worries

This direct involvement can mean the difference between a payout that covers your losses in full or a drawn-out dispute that puts your cash flow and reputation at risk.

Adapting to Changing Regulatory and Environmental Risks

It’s no secret that insurance isn’t static. New laws, localised weather events, or shifts in tenant-landlord policies can all disrupt your risk profile.

For property managers in Australia, several recent developments have shifted the dial:

- Climate-related claims (especially for storms, floods and bushfires) are leading to stricter policy requirements and higher premiums

- Regulatory changes around rental minimum standards and safety obligations are affecting what must be included in landlord and strata insurance

- Ongoing economic shifts are impacting the solvency of tenants, increasing rent default risks

A broker who keeps their finger on the pulse will flag these and adjust your policies before you’re exposed. That saves time, money, and a world of stress in the long run.

Building a Long-Term Relationship

Many property professionals see insurance as a once-a-year admin chore. The problem is that risk doesn’t recognise calendar reminders. Properties get renovated, tenants change, and neighbourhood risk profiles are never static.

By working closely and openly with a diligent broker, you benefit from:

- Ongoing reviews and updates tailored to your current portfolio

- Alerts whenever the market or regulatory landscape shifts

- Targeted guidance on steps to take before or after an incident

It’s about forming a partnership that evolves as you do, rather than a transactional annual checkbox.

What does a Day-to-Day Relationship Look Like?

The best relationships with insurance brokers aren’t built on emergencies alone. Here are just some ways brokers keep property managers ahead of the curve:

- Scheduling regular check-ins to review your portfolio’s risk profile

- Providing plain-English breakdowns of fine print whenever you need

- Advising on risk mitigation upgrades, from improved locks to new compliance checklists

- Alerting you to relevant insurer policy changes or more competitive offers

These small but methodical touches save time and prevent loss. They also build mutual confidence, which matters when you’re managing not just property but also owners’, tenants’, and investors’ trust.

Key Questions Every Property Manager Should Ask Their Broker

To make the most of your broker relationship, there are some important questions to include in your next conversation:

- What are the current key risks in my portfolio, and how are they covered?

- Have there been any recent legislative or insurer policy changes I need to be aware of?

- How do you handle claims, and what support can I expect if I need to submit one?

- Can you explain my policy’s exclusions or limitations in simple terms?

- Are there any upgrades, discounts, or enhancements we should consider this year?

A diligent broker welcomes these questions and won’t rush their answers.

Choosing the Right Broker

Not every insurance adviser is created equal. Some focus primarily on new business and commissions, while others are motivated by the long-term value built through trust, performance, and insight.

Look for these signals of genuine diligence:

- Industry experience specific to property and strata risk

- Attentive, timely communication — no disappearing acts

- Proactive touchpoints, even when there’s no immediate renewal or claim

- Detailed market knowledge and transparent fee structures

When these qualities are evident, you gain more than just a policy document. You secure peace of mind, greater control, and a clear path through the ongoing complexity of property insurance.

The property sector is demanding enough. With a diligent insurance broker by your side, you tip the odds in your favour by ensuring the unforeseen is as managed and mitigated as possible — and your business, investments, and clients remain secure, no matter what tomorrow brings.

Comprehensive Construction and Trades Insurance Plans for 2025

Comprehensive Construction and Trades Insurance Plans for 2025

Whether you’re a builder, electrician, plumber, or run a carpentry business, insurance isn’t just a formality. On every worksite, unexpected incidents can disrupt projects, threaten finances, and impact reputations. Reliable insurance offers not just a safety net but a tool for growth and stability in an industry where risks are woven into daily operations.

Builders and tradespeople face unique challenges. Precision work, tight deadlines, hazardous materials, and valuable tools leave no room for complacency. Heavy machinery, unpredictable weather, and the ever-present risk of injury can create a complex web of liability. Insurance tailored to the building and trades sector helps turn risks into manageable obstacles.

Why Construction and Trades Professionals Need Specific Cover

General business coverages often fall short for those who construct, repair, and install. Policies designed for hairdressers or retailers simply do not account for the daily exposure to high-value projects, occupational hazards, and specialist equipment that tradies face. Industry-specific insurance provides cover built around your business’s real risks, not a broad-brush approach.

Let’s consider just a few of the realities:

- Falling objects and on-site accidents can threaten lives and livelihoods.

- Faulty workmanship might lead to costly rework or even litigation.

- Unattended tools and machines are tempting targets for thieves.

- Delays caused by weather, supply issues, or subcontractor problems can put contracts in jeopardy.

Insurers focused on construction and trades typically consult closely with businesses to match cover to the risks at hand.

Core Types of Insurance Tradies Should Consider

One size rarely fits all, but certain core coverages are essential across most trades. Choosing the right mix can be the difference between a minor setback and a financial disaster.

Public Liability Insurance

Arguably the linchpin of any construction or trades cover. This protects you against claims from third parties for property damage or injury caused by your work. Even the most skilled professionals can’t predict every mishap — a stray ladder, a split water pipe, or a client tripping over tools can trigger claims worth thousands or even millions.

Contract Works Insurance

Projects don’t always go to plan. Contract works insurance (sometimes called ‘construction all risks’) is designed specifically to protect against accidental damage or loss to structures and materials during a build. It covers many events beyond your control: storm damage, burglary, or fire during the build phase.

Tools and Equipment Insurance

For many tradespeople, tools are their livelihood. Whether transporting equipment between sites or locking up overnight, theft and accidental damage are constant threats. Tools insurance gives reassurance that your business can carry on if the worst happens.

Workers’ Compensation

This isn’t just important - for many employers, it’s mandatory. Workers’ compensation covers costs if workers are injured or made ill through work, providing wages, medical expenses, and rehabilitation.

Professional Indemnity Insurance

Clients expect projects to be completed to a high standard. If your advice or work is later alleged to have caused financial loss (perhaps through faulty design or installation), indemnity cover can absorb the legal and compensation costs.

Commercial Vehicle Insurance

Tradies depend on utes, vans, and trucks to move between jobs and transport materials. Accidents, vandalism, or theft of a vehicle can halt work in its tracks. Specialised commercial vehicle cover addresses the unique risks of construction and trades transport.

A Snapshot Comparison of Key Covers

Each type of insurance covers different risks. Here’s a simplified reference for what’s protected by the main categories.

| Insurance Type | Typical Coverage | Scenarios Covered |

|---|---|---|

| Public Liability | Injury/property damage to third parties | Client slips, property damaged |

| Contract Works | Loss/damage to building and materials during construction | Storm, theft, site fire |

| Tools & Equipment | Theft, fire, accidental damage to tools/machinery | Tools stolen from van or worksite |

| Workers’ Compensation | Worker injury or illness (wages, medical bills) | Onsite falls, trenched injuries |

| Professional Indemnity | Legal defence/costs tied to alleged poor advice or work | Faulty design, missed compliance |

| Commercial Vehicle | Damage/loss involving work vehicles | Crash on way to job, theft |

Each business’s needs will differ, but skipping any of these creates potential blind spots.

Factors Driving Insurance Costs

Many business owners ask why premiums can be higher in construction compared to some other fields. Several factors influence the costs:

- Size and complexity of projects handled

- Total payroll or number of employees

- Types (and value) of equipment used

- Claims history and risk management measures

- Location and security of work sites

A builder overseeing multi-storey commercial projects will pay more than a solo painter handling residential touch-ups, reflecting the risk that insurers are asked to shoulder.

The Role of Risk Management and Compliance

Savvy insurers reward safe practices. By maintaining rigorous safety standards, providing staff training, and following legal compliance, construction businesses may not only reduce the likelihood of claims but can also see lower premiums.

Adopting clear site protocols and investing in secure storage for equipment signals to providers that a business takes risks seriously — and that can translate into savings.

Some practical steps that can support your insurance application:

- Schedule regular tool audits and equipment safety checks.

- Maintain clean, signed, and well-lit worksites.

- Use site diaries and detailed project records.

- Provide sufficient training on tools and vehicles.

- Keep security systems and locks up to date.

A strong focus on prevention also means less disruption, more consistent project delivery, and a safer environment for all.

Industry-Specific Add-Ons and Tailored Solutions

Every trade is different, from roofers exposed to height risks to plumbers at risk of water escape or electricians working with live circuits. Insurance flexibility is vital. Many providers offer bolt-on covers or tailored extensions, such as:

- Plant and machinery: Coverage for hired-in or owned assets.

- Income protection: Safeguards your wages if illness or injury prevents you working.

- Product liability: Specifically focused on manufactured or installed products that could cause harm after installation.

- Environmental liability: Covers accidental pollution or environmental damage linked to building activities.

- Cross liability: Essential for joint ventures and larger projects with multiple parties at risk.

Some businesses may opt for annual policies, while others take out single project or contract-specific cover depending on the size and scope of work.

Questions to Ask When Arranging Insurance

Many tradies simply renew each year without careful review. Taking time to sit down with a knowledgeable broker can ensure you’re getting genuine value. Key questions worth asking include:

- Has my business changed in size, scope, or specialisation this year?

- Am I meeting all contractual and legal insurance requirements for each job?

- Are all subcontractors and third parties sufficiently covered?

- Do I have the right level of cover for equipment, materials, or vehicles?

- Have claims (or near misses) indicated areas where more cover or tighter safety is needed?

Open communication with your insurer can help avoid grey areas or unwelcome surprises at claim time.

The Hidden Value of Strong Insurance

Robust insurance doesn’t just cover losses. It can open up opportunities to win larger projects, meet client contractual obligations, and satisfy bank or financier demands for cover.

Some benefits go beyond risk transfer:

- Potential to negotiate better payment terms with suppliers

- Boosted confidence when tendering for ambitious contracts

- Smoother dispute resolution, with legal support built in

- Attracting high-quality employees who want a safe, stable workplace

Professional reputation is enhanced by showing clients and partners that your business takes its responsibilities seriously. In a competitive market, comprehensive cover can be a positive differentiator.

Keeping Cover Current as Your Business Grows

The construction and trades sector doesn’t stand still. As you develop new skills, acquire equipment, or grow your workforce, your insurance should move in step.

Many successful operators set a calendar note to review policies before every renewal or major contract. Simple changes—updating a vehicle, hiring extra staff, expanding into new areas—need to be reflected in your coverage to avoid underinsurance. The right insurance advisor doesn’t just sell a policy and disappear; they act as a long-term partner as your business expands.

Regular conversations and honest disclosures help ensure that you aren’t left exposed. In a sector where change is constant, keeping insurance tightly matched to activities is part of staying resilient, professional, and open to new opportunities.

Guide to Different Insurance Policies

Guide to Life, Car, Health, Home, Travel & Pet Insurance

Insurance often seems like a tangled web of policies, jargon, and unforeseen scenarios. Yet, at its core, insurance is about providing confidence that, should adversity strike, you can weather the storm without starting again from scratch. Cover of all kinds offers a safety net, but not every policy fits every need. Understanding the different forms of insurance can empower you to make choices aligned with your own circumstances, values, and aspirations.

Let’s unpack six of the main types of insurance commonly encountered: life, car, health, home, travel, and pet. Each has its own role and speaks to different priorities and life events.

Life Insurance: Securing Futures

Life insurance is often a topic people avoid—sometimes out of superstition, other times because it raises uncomfortable questions. At a practical level, though, life insurance is about peace of mind, ensuring those who depend on you are shielded from financial turmoil should the unforeseen occur.

Two Main Forms:

- Term Life Insurance: Covers you for a specified period (often 10, 20, or 30 years). If you pass away during this term, a fixed lump sum is paid to your beneficiary. Generally more affordable, this option is widely chosen by those looking to protect loved ones through the years of raising children or paying off a mortgage.

- Whole (or Permanent) Life Insurance: Lasts your entire lifetime and often accumulates cash value over time. This can be used as an investment or even borrowed against. It comes at a higher cost but includes lifelong protection.

Why do people buy life insurance?

- To provide for family members if income is lost.

- To cover debts, funeral costs, and final expenses.

- To leave a legacy or charitable donation.

A table can help distinguish some of the core differences:

| Feature | Term Life | Whole Life |

|---|---|---|

| Coverage Length | Fixed term | Lifetime |

| Premiums | Lower initially | Higher |

| Cash Value | No | Yes |

| Payout on Death | Yes (if within term) | Yes (any time) |

Car Insurance: Protecting Your Journey

Anyone who drives in Australia is legally required to hold some form of car insurance. But beyond the basics, there’s a range of policies, each providing a different degree of protection for different risks.

The Main Types:

- Compulsory Third Party (CTP): Also known as the ‘Green Slip’ in NSW, this covers injuries to people (not property) that you might cause while driving.

- Third Party Property: Covers you for damage you might cause to another person’s property, such as their car or fence.

- Third Party Fire and Theft: Adds cover if your car is stolen or damaged by fire.

- Comprehensive: Provides the widest protection, covering your car as well as others’ property, regardless of who is at fault.

The choice here depends a lot on the age and value of your car, your budget, and how much personal risk you feel comfortable carrying.

Health Insurance: Guarding Your Wellbeing

Health is unpredictable, and while Australia’s Medicare system covers many essential services, private health insurance fills the gaps, especially around hospital stays, elective procedures, and specialist treatments.

Options Available:

- Hospital Cover: Pays for accommodation and treatment as a private patient in either a public or private hospital.

- Extras Cover: Assists with costs of services not covered by Medicare, like dental, optical, physiotherapy and alternative therapies.

- Ambulance Cover: Important, as ambulance costs aren’t always fully covered in every state and territory.

Private health insurance can also help you skip public hospital waiting lists for particular treatments, and it offers flexibility around which doctor or hospital you use.

Some key reasons Australians take out private health insurance:

- More control over treatment and choice of practitioner.

- Coverage for services not included under Medicare.

- To avoid the Medicare Levy Surcharge for higher-income earners.

Home Insurance: Safeguarding Where You Live

Home is more than bricks and mortar; it’s the backdrop to life’s biggest moments. Protecting your home and its contents protects stability itself.

Two Branches:

- Building Insurance: Covers damage to the structure itself—the walls, roof, floors, built-in fixtures.

- Contents Insurance: Covers loss or damage to your possessions inside the home: furniture, electronics, clothing, jewellery and valuables.

Many people combine the two. If you own your home, banks will require building insurance as a condition of your mortgage. Renters, on the other hand, will often just opt for contents cover.

Risks these policies might address include:

- Fire

- Storms and floods

- Theft or vandalism

- Accidental damage

Reviewing the fine print is vital, as inclusions and exclusions vary greatly. For instance, in flood-prone regions, certain forms of water damage might not be covered unless you select specific options.

Travel Insurance: Cover for the Unexpected

Travel brings adventure and connection, but it also exposes you to risks far from home. Out-of-pocket costs for accidents, illness, trip cancellations or theft while travelling can quickly escalate.

Travel insurance policies are typically tailored for:

- Medical and Hospital Cover: Essential, given overseas medical costs (particularly in the USA) can be prohibitively expensive.

- Trip Cancellation and Interruption: Refunds your prepaid costs when trips are delayed or can’t be completed.

- Baggage and Belongings: Covers theft, loss or damage.

- Personal Liability: Protects you if you are held responsible for injuring someone or damaging property.

Many Australians who travel domestically assume their normal health cover applies. This isn’t always the case, especially for events like missed flights or lost luggage.

A short checklist for comparing travel insurance might include:

- Medical benefits and exclusion clauses

- Pre-existing medical condition coverage

- Adventure sports coverage (if needed)

- Excess levels

Pet Insurance: Looking After Four-Legged Family

For animal lovers, pets are part of the family. Pet insurance helps manage the costs associated with vet bills, accidents, and sometimes even routine care.

Categories of Cover:

- Accident Only: Generally the most affordable, covering injuries such as snake bites, car accidents, or broken bones.

- Accident and Illness: More comprehensive, also including cover for diseases, infections, cancer treatments and more.

- Comprehensive (with Routine Care Add-On): Can include vaccinations, microchipping, dental treatments, tick prevention and more.

Vet costs can be substantial, particularly as animals age and chronic conditions emerge. Many policies have waiting periods and specific exclusions, especially around pre-existing conditions, so it’s vital to check the finer details before buying.

Some Key Considerations When Choosing Insurance

No two households are identical, and the right cover for you will depend on your circumstances, stage of life, and personal priorities. Here’s what to weigh:

- Budget vs. Peace of Mind: Higher cover means higher premiums but greater security.

- Policy Inclusions/Exclusions: Always check what is, and isn’t, covered.

- Waiting Periods: Some benefits aren’t available immediately.

- Excesses: Higher excess may reduce your premium but mean a bigger upfront payment if you claim.

- Bundling Discounts: Many insurers offer savings if you buy multiple policies.

Comparing Insurance Types at a Glance

The following table provides a snapshot across the main types of insurance, showing what they generally cover:

| Insurance Type | Who/What is Covered | Typical Benefits | Who Usually Needs It |

|---|---|---|---|

| Life | Your life, your family | Lump sum payout to beneficiaries | Those with dependants, mortgage |

| Car | Car, others’ property | Repairs, replacement, liability | All drivers (compulsory element) |

| Health | Your health | Medical, hospital, extras | Anyone seeking greater choice/cover |

| Home | House & contents | Repair/replacement of home/possessions | Home owners, renters |

| Travel | Traveller, belongings | Medical overseas, trip cancellation, lost items | Anyone travelling afar |

| Pet | Your pet | Vet bills, accidents, routine care | Pet owners wanting cost protection |

Making Insurance Work for You

Insurance isn’t just a grudge purchase or a regulatory requirement. Thoughtful, tailored cover is a safeguard for the things in life you value most — and a tool to help you pursue bigger dreams without unnecessary worry.

Choosing insurance isn’t about avoiding risk entirely. It’s about removing the sting from life’s shocks so you can get on with living. By considering what’s important to you and weighing up your own risk appetite, you’ll find policies that augment your sense of security, letting you look ahead with confidence.

Taking the time to compare, question, and tailor your cover ensures that when you need support most, the groundwork has already been laid. Insurance, at its best, opens the door to opportunity.

Demystifying Insurance Complexity

Demystifying Insurance Complexity: A Clear Guide to Simplifying Coverage

Picture yourself faced with a stack of policy documents thicker than a phone book. Pages and pages of inclusions, exclusions, percentages, conditions, and legalese. There's the pressure of making the right call—because it’s not just about money but about protecting your lifestyle, home, family, or business. So why is insurance still so confounding, even though it’s supposed to be a safety net?

The answer often lies in how these products are presented. The raft of options, technical terms, and jargon have created an environment where even the most diligent clients feel like they’re always missing something. This uncertainty can lead to decision fatigue, procrastination, or worse, policies that don’t genuinely reflect what someone needs.

There’s a better way.

A Personalised Approach—Listening First

It all starts with tuning out the unnecessary complexity and shifting focus entirely onto the individual person or business. No two clients are the same, so a one-size-fits-all approach will always fall short. Instead, understanding what truly matters to someone, be it peace of mind for a young family, risk mitigation for an entrepreneur or safeguarding a nest egg for retirees, should be the very first step.

Instead of beginning with products, start by listening:

- What worries keep you up at night?

- Are there unique assets or dependants involved?

- Have you had insurance before, and were there frustrations?

- Are there specific events you’d like the policy to protect against?

This conversation removes the abstraction and grounds the entire discussion in the reality of the person in front of you.

Breaking Down Jargon

Terms like “benefit period”, “aggregate limit”, “excess”, or “declaration page” can cloud judgement. An important part of simplifying insurance is translating jargon into plain language, stripping out ambiguity and focusing on outcomes.

When introducing a new concept:

- Use analogies people already understand (e.g. “Think of excess like the first part of a repair bill you pay before your insurer contributes”).

- Avoid acronyms unless necessary, and if used, define them clearly.

- Pause often and check if further explanation is required.

This two-way dialogue not only clarifies but builds trust. Clients know they can ask a question at any time and receive a straight answer.

Transparent Comparisons

Side-by-side comparisons of policy features, rather than sales pitches, help demystify choices. Visual tools are extremely effective here—a simple table can make a world of difference:

| Feature | Policy A | Policy B | Policy C |

|---|---|---|---|

| Sum Insured | $500,000 | $400,000 | $600,000 |

| Excess | $500 | $1,000 | $500 |

| Trauma Cover | Yes | No | Yes |

| Premium (monthly) | $45 | $38 | $50 |

| Family Discount | 5% | None | 10% |

Clients can quickly see what matters to them and weigh the trade-offs. Is it worth a bit more for extra trauma cover? Does a higher excess really justify a lower premium?

Illustrating Real-World Scenarios

Insurance isn’t just about numbers on a page. Bringing policy choices into the real world gives context and helps clients visualise how a policy would function in their life or business.

Consider scenarios like:

- “If your home suffers storm damage, here’s exactly how Policy A will respond vs Policy B.”

- “Let’s walk through what happens if you need to make a claim for income protection.”

- “Here’s what you’d pay out of pocket for a hospital admission under both options.”