Comprehensive Guide to Residential Strata Insurance in NSW

Key Takeaways

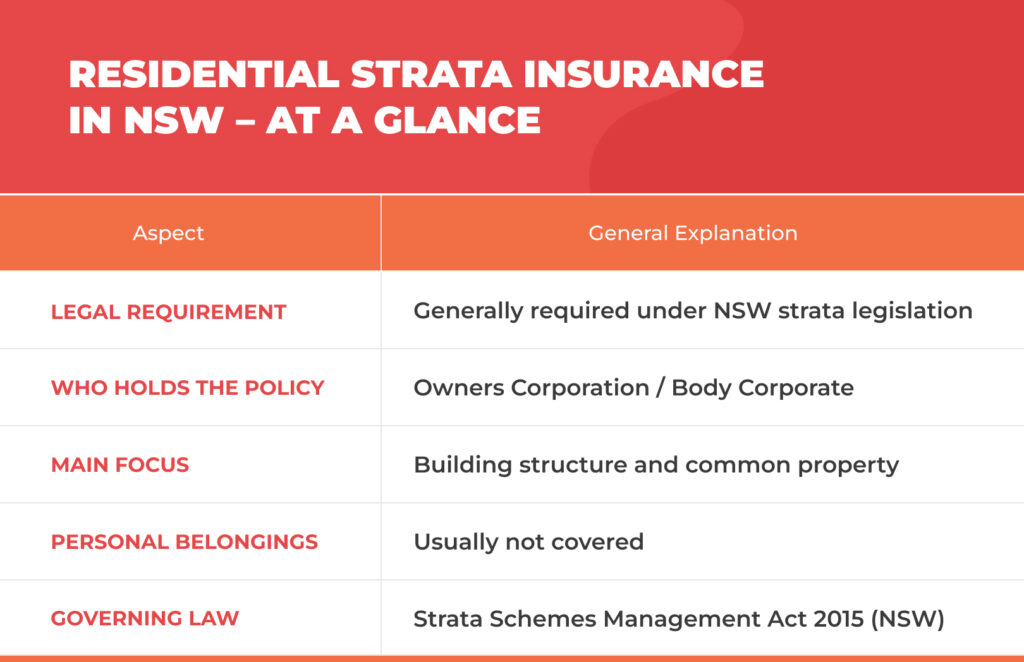

- Residential strata insurance NSW is in most cases a legal requirement for any strata-titled property as per NSW legislation.

- Normally, coverage is focused on communal facilities, common areas, and the building, with risks considered rather than individual contents.

- The policy features and optional covers may vary depending on the characteristics of the strata scheme and the specific insurer’s policy terms and conditions.

- In fact, a professional can help with documentation and compliance requirements within the scope of general information or services permitted under Australian law.

Residential strata living is one of the most popular features of the New South Wales lifestyle, particularly in apartment blocks, townhouses, and shared residential developments. Because more parties are involved, such as lot owners, committee members, and a strata manager, the insurance arrangements are usually more complex than those for a typical home. This guide explains residential strata insurance in NSW using straightforward, general, and law-friendly language so that readers can get a clear and accurate comprehension.

This information is general in nature and does not take into account your personal objectives, financial situation, or needs.

Understanding Residential Strata Insurance in New South Wales

Residential strata insurance covers shared risks arising out of strata titled properties. In NSW, such arrangements are regulated by law and are generally implemented by a strata company or body corporate, sometimes with assistance from a professional property manager.

What Is Strata Insurance?

Strata insurance is a policy that primarily covers strata title properties. It is usually mandated under the Strata Schemes Management Act 2015 (NSW). The insurance can cover the property's structure and amenities, such as common areas and conveniences available to all residents. Insurance generally does not cover the personal belongings of individuals living in the units, known as 'lots'.

Strata insurance is, in most cases, a separate insurance from the insurance an individual takes for their home, which generally covers the stuff inside the home.

Who Benefits From It?

Residential strata insurance is pretty much a common theme for:

- House owners residing in strata dwellings

- The body corporate who ensures that all obligations are met

- Strata managers are responsible for the daily administration

- The members of the committee and the office bearers who represent the scheme

Start your Quote today!

Key Features of Residential Strata Insurance

Having a clear idea of what is typically covered and what might be optional will definitely help you understand the structure of these policies.

Coverage Inclusions

Although the exact details differ depending on the provider and risk profile, residential strata insurance is generally concerned with:

- Home Building items and the physical building structure

- Common area contents, such as shared fixtures

- Storm, water, accidental, and malicious damages

Insurers typically do not cover problems caused by wear and tear, as these are generally considered maintenance issues.

Optional Covers and Extensions

Some optional covers that may be available under certain policies include:

- Machinery breakdown cover (e.g. lifts, shared pumps, or air-conditioning units)

- Catastrophe insurance for major insured events

- Pools and related infrastructure protection

The availability and scope of optional covers depend on the insurer, underwriting criteria, and policy terms and conditions.

Additional Benefits Commonly Considered

Residential strata insurance policies may also include, subject to the policy:

- Accommodation in case of necessity and Loss of rent after insured events

- Cover for volunteer workers helping the strata scheme

- Office Bearers liability and Legal Defence Expenses

- Property Damage Liability in the case of shared areas

In some cases, certain administrative or regulatory costs may be included, depending on the policy wording.

The Role of Strata Insurance Specialists

Many schemes engage a strata insurance specialist to provide support with understanding and administration, given the regulatory environment and diverse building designs.

Why an Insurance Broker Is Usually Involved

An insurance broker may assist by providing general information only, unless otherwise disclosed, including:

- Identifying the general advice boundaries

- Helping with insurance quotes and a Strata Insurance quote

- Ensuring Target Market Determination alignment

- Offering access to compliance tools and data insights

Before arranging any insurance, brokers generally provide a Financial Services Guide (FSG) and refer clients to the relevant Product Disclosure Statement (PDS), which should be reviewed carefully before making any decisions.

Industry Partnerships and Market Structure

Some brokers operate within broader industry networks. For example, VIM Cover is a member of the Steadfast Network, which is associated with the Steadfast Group Ltd, and may work with specialist underwriting agencies such as CHU Underwriting Agencies Pty Ltd.

This information is provided for general market awareness only and does not constitute a recommendation or endorsement of any specific broker, insurer, or underwriting agency.

Such agreements can facilitate a wider range of underwriting skills for strata properties in NSW and South Australia. Various entity codes may include ABN 18 001 580 and ABN 98 073 659 677, depending on the entity involved.

Steps to Secure the Best Strata Insurance Policy

Important Considerations for Strata Committees

Before reading the insurance policy or renewing it, a committee generally takes into account:

- The scheme’s total financial health

- Age of the building, type of construction, and communal facilities

- Claims record and risk profile changes

Sometimes, a committee member may coordinate with a strata manager to ensure that the documentation stays in line with the legislation and insurer requirements.

FAQs

Q1. Is residential strata insurance compulsory in NSW?

A1. Generally, the legislation requires that strata schemes in NSW maintain insurance for the building and the common property.

Q2. Does strata insurance replace home insurance?

A2. Strata insurance usually covers common/shared property, whereas home insurance covers items inside individual lots.

Q3. Are washing machines included in strata insurance?

A3. It appears that fixed infrastructure could be treated differently from appliances such as washing machines, which are usually considered personal property. Coverage depends on how items are defined in the policy wording.

Q4. Who is responsible for the strata scheme insurance?

A4. It is typical for the body corporate or strata manager to arrange this, and at times they may be assisted by an Insurance Broker acting within the scope of their authorised services.

Comprehensive Guide to Residential Strata Insurance in QLD

Key Takeaways

- Residential strata insurance in QLD is mainly about insulating common property and shared building elements in strata schemes.

- Insurance policies can offer different coverage, so it is a good idea to check the relevant Product Disclosure Statement and Target Market documents.

- Strata insurance is not simply a type of Home Insurance or Landlord Insurance; it differs in both its make-up and its aims.

- Industry participants may provide general information about types of general insurance without taking into account individual circumstances.

Residential strata insurance plays an established role in protecting and managing shared living environments throughout Queensland. Sometimes, even a small-unit complex or a multi-storey residential development can be a strata property. Besides multiple owners, it involves shared responsibilities, common risks, and key differences from single-family homes.

Understanding residential strata insurance in QLD helps strata owners understand the framework. It also explains the cover and exclusions.

This guide provides general information only. It is not financial product advice and does not take into account individual goals, financial situations, or needs.

Readers should refer to the relevant Product Disclosure Statement (PDS), Target Market Determination (TMD), and Financial Services Guide (FSG) before choosing an insurance product. They should also seek independent professional advice if necessary.

What Is Residential Strata Insurance?

A Body Corporate usually organises residential strata insurance for strata-titled properties such as apartments, duplexes, and townhouses. Instead of a single dwelling, this insurance usually covers the strata building, common areas, and shared facilities. These facilities are used by multiple occupants.

Residential strata insurance in Queensland generally refers to insurance for strata properties regulated under the Body Corporate and Community Management Act. This act sets out the insurance requirements for strata schemes. Even though coverage varies, policies are usually for the property insured, not for the personal belongings of individual lot owners.

Start your Quote today!

Understanding Strata Insurance Basics

A key characteristic of residential strata insurance QLD is that it generally insures common property and areas. Examples include hallways, lifts, stairwells, gardens, driveways, and shared amenities such as swimming pools. The idea is to protect collectively owned and maintained places, even though individuals do not privately hold them.

Depending on the policy wording, strata insurance may cover insured events such as accidental damage, storm damage, and water damage. The extent of cover is determined by the inclusions and exclusions listed in the policy documents.

In fact, most strata insurance policies include a public liability section that covers injuries or property damage in common areas. Consequently, this kind of cover is especially necessary when visitors, residents, or even volunteers use shared facilities.

Why Residential Strata Insurance Is Relevant for Strata Title Properties

Queensland legislation imposes a general obligation on bodies corporate to ensure appropriate insurance is in place for their strata schemes. This insurance mandate reflects the co-ownership aspect of strata buildings and the consequent need to manage risk collectively in Australian strata settings.

Typically, residential strata insurance covers the risks of the physical building, including permanent fixtures and contents in common areas. In contrast, it differs from the content insurance policy arrangements held by individual lot owners.

Although strata insurance applies to communal property, individual lot owners may hold separate Home Insurance or Landlord Insurance policies. These policies can cover personal contents, floating floors, or alterations not classified as common property under strata legislation and scheme by-laws.

Key Inclusions Commonly Found in a Strata Insurance Policy

Coverage for Strata Properties

Typical inclusions might generally be:

- The physical structure of the building and the specified building sum

- Contents in the common area, like lights, fixtures, or communal equipment

- Rent loss due to an insured event that disrupts tenancy arrangements

Additionally, certain insurance policies can highlight Office Bearers' cover or safeguards. This protects committee members when they perform their official duties.

Additional Coverage Areas

Optional sections may concern the following, depending on the insurance products:

- A machinery breakdown that affects the shared systems

- Property damage cover is limited to the involvement of shared facilities

- Clearly defined liability issues relating to voluntary workers

The availability of coverage depends on the policy terms and the insurer's Target Market.

How Insurance Premiums Are Commonly Influenced

Factors Influencing Insurance Premiums

One factor alone is rarely the reason behind the increase or decrease of insurance premiums for residential strata in QLD. The insurance company may consider the claims made on the strata property over the last few years, the strata's risk profile, and the value of your home as part of the whole building.

Moreover, factors such as points of cover, previous loss events, claims history, and building characteristics may also be assessed. For this reason, premium rates differ between insurers and policy types.

Reading the Product Disclosure Statement

The relevant PDS would cover what is included and excluded, the limits, and the claims procedure. Going over this piece helps the parties involved clarify the definition of the cover and when it applies.

On the other hand, the Financial Services Guide and the like clarify the delivery of insurance services and the role of intermediaries. Collectively, such documents constitute the wider disclosure framework under Australian financial services law.

Strata Management and Insurance Responsibilities

Role of Strata Managers and Committees

Strata management is a system usually composed of a strata manager, the strata committee, and the owners of individual lots. They share several responsibilities, including ensuring the body corporate has insurance, complying with strata scheme regulations, and handling collective decision-making processes.

In most cases, good strata management is a matter of committee members and residents talking regularly about insurance options, claims, and any changes introduced by a new policy.

Secure Your Strata Property with the Right Insurance

This guide focuses on Queensland. However, residential strata insurance frameworks in New South Wales and South Australia may differ due to variations in legislation and regulations.

The specific needs and characteristics of local areas, building types, and the use of strata-titled properties influence insurance arrangements.

This content does not constitute financial product advice and does not take into account individual objectives, financial situations, or needs.

FAQs

Q1. Is residential strata insurance the same as a Home Insurance policy?

A1. No. A Home Insurance policy usually covers a single dwelling, while strata insurance generally covers shared building elements.

Q2. Does strata insurance cover personal items?

A2. Personal items and belongings are typically covered under individual contents insurance, not strata insurance.

Q3. Who arranges residential strata insurance in QLD?

A3. The Body Corporate generally arranges it on behalf of the strata schemes.

Q4. Are all events automatically covered?

A4. Coverage depends on policy terms, insured events, and exclusions outlined in the Product Disclosure Statement.