Understanding Public Liability Insurance Costs in 2026

Public Liability Insurance is one of the essential types of business protection that has received considerable attention over the years, and its significance in 2026 is even higher. Over time, an increasing number of sole traders, small business owners, and service providers have ventured into public places and had direct contact with their clients. In such a scenario, the risk of the businesses being sued for property damage and personal injury is at a high level. A business owner can make well-informed judgments on how to safeguard their company by understanding the cost of public liability insurance and the factors that significantly influence those prices.

Key Takeaways

- The cost of coverage in 2026 will vary widely depending on your industry, turnover, location, and level of risk exposure.

- Small business owners, sole traders, and other businesses in higher-risk industries need to prioritise adequate coverage first and foremost.

- Finding the right providers for you and access coverage that suits your protection needs means that you will have the right balance of protection at the correct cost.

This blog explores public liability insurance, a type of insurance that benefits companies. The main description of the coverage, the factors affecting the premium, and the premium forecast for 2026 have also been discussed.

Why Businesses Need Public Liability Insurance

In any case, there are always possibilities of something going wrong with the public, even if you are operating carefully. Imagine that a customer falls on a wet and slippery floor, a contractor damages a client's property without realising it, or a minor mistake leads to a huge claim. These problems can escalate into money disasters if there is no insurance.

Protecting Against Financial Losses

Covers property damage and personal injury

If a customer, for instance, gets hurt at your business location or, by chance, your work damages someone else’s property, a claim resulting from these incidents might be costly. Public liability insurance protects the policyholder against such cases, paying the legal costs, may cover medical expenses if included in a successful third-party claim, and taking care of the repair without the amount being a burden on the business.

Essential for small business owners, sole traders, and construction companies

Smaller enterprises and individual traders usually lack the financial resources to cover significant claims. Companies in the building sector, workers in the trades, and similar professionals are particularly vulnerable due to the nature of their work.

Mitigates risks from negligent activities and legal liability.

Although all possible safeguards may be implemented, there is still a possibility that an accident or oversight may occur. It is also typical for courts to concentrate on the results rather than the motives, thus companies can still be held responsible. A company can protect itself with public liability insurance, which reduces the risk by covering not only damages but also legal defence costs. This way, management can focus on ensuring the business continues to function after such an event.

Who Should Get Public Liability Insurance?

Risks certainly differ among various businesses to some extent. However, any company that has contact with clients or the public will benefit from considering public liability insurance. The size of your business is less important than what you do. If you are involved in any kind of outdoor activity, then not only is the risk present, but also the need for protection.

- Businesses often occupy various public areas, including malls, construction worksites, and event venues.

- Some industries, such as professional services or trade, include advertising agencies, management consulting firms, and the skilled trades.

- Local small business entrepreneurs who have face-to-face interactions with customers and the public.

- Particular attention must focus on hazardous firms, such as those where a mistake, exposure to boiling liquid, or food poisoning could result in a series of claims.

- These are the businesses that pose a danger; for example, a mishap, hot liquid, or food contamination can lead to a chain of claims.

What Influences the Cost of Public Liability Insurance?

Insurance premiums are never uniform for all customers. The amount a café needs to pay for its insurance can be significantly different from what a plumbing contractor or a marketing agency needs to pay. The reason is that insurers consider multiple factors when determining your premium, including the size of your business and the associated risks within your industry.

Key Factors That Affect Premiums

- Business size and turnover: Larger businesses with higher revenue usually pay more, as their exposure is greater.

- Industry type: A marketing agency may pay less than a restaurant, where food poisoning claims are more common.

- Location: States such as Western Australia or the Northern Territory may have different pricing due to their unique risk environments.

- Level of cover: The higher the amount of public liability cover, the higher the premium. Adding extra insurance products will also influence cost.

Industry-Specific Risks

- Hospitality establishments must contend with the risk of burns from hot liquids or food safety issues.

- Workers in trades and contracting businesses are at risk of being exposed to claims for property damage and personal injury in the places where they work.

- Even service providers like consultants need insurance because visitors to offices or events where clients are present could get hurt.

How Much Does Public Liability Insurance Cost in 2026?

Public liability insurance costs in 2026 will be influenced by several factors, including the general rise in prices, changes in government regulations, and shifts in the risk environment, resulting in varying costs. Besides the differences in industries, firms will also experience changes in their locations due to the different states, insurance companies, and the share they want to cover.

Average Costs and Insurance Options

Although there is an excellent range of costs, a majority of small businesses in 2026 will be able to anticipate that their premiums may start at a few hundred dollars per year for the basic cover as a minimum. For industries with higher risks, the premium can reach several tens of thousands of dollars per year.

Several factors, like stamp duty, state taxes, and the amount of cover requested, determine the final number. Small business owners can select customised plans that match their financial condition, securing them without depleting their funds.

How to Get a Public Liability Insurance Quote

- Consult with experts – Business insurance specialists can assess your industry, risks, and needs.

- Compare policies online – Many insurers allow side-by-side comparisons of public liability policies.

- Request documentation – Always ask for complete details, including policy wording and the certificate of currency, to confirm coverage levels.

What Does Public Liability Insurance Cover?

Many business owners believe they have a solid grasp of the coverage provided by public liability, but then a situation arises, and they discover that several risks are not covered.

Knowing what a standard policy comprises allows you to stay covered in areas that may be costly if you have no insurance, and also gives you peace of mind when dealing with the public.

Third Party Claims

Policies generally cover:

- Property damage caused by your business activities

- Personal injury to members of the public

- Legal defence costs and associated expenses

Additional Insurance Options

Businesses often combine public liability with:

- Product liability (covering issues with goods sold)

- Trade insurance for contractors

- Workers’ compensation

- Home insurance or car insurance for business-related assets

- Income protection and life insurance for broader security

Choosing the Right Public Liability Policy

It is well known that multiple insurers offer public liability insurance, and numerous business insurance packages are available on the market. As a consequence, choosing the proper one can become an overwhelmingly difficult task. The most efficient approach is to analyse business needs first and then evaluate providers familiar with your field of work.

Assessing Business Needs

The right policy depends on your:

- Type of business and work environment

- Risk exposure from daily activities

- Financial situation and capacity to pay liability premiums

Although sole traders in the construction industry may require less insurance than large companies, it remains essential for both to have sufficient cover to avoid financial burden in the event of a claim.

Finding the Best Insurance Provider

It is not that every insurance company provides the same value. Investigate companies that specialise in small business packages or have experience with specific industries. Utilise the buying power of your group, such as a trade association, to access reasonably priced rates.

Looking for reliable public liability insurance that can truly safeguard your small business?

Licensed insurance brokers such as VIM Cover can assist with tailoring insurance that fits the unique needs of small businesses located anywhere in Australia. Whether you require only basic coverage or a comprehensive policy, our skilled brokers will guide you towards finding an ideal solution that suits both your needs and budget.

You can obtain quotes from licensed insurance brokers such as VIM Cover.

FAQs

Q1. What is the average public liability insurance cost for small businesses in 2026?

Small businesses typically allocate between a few hundred and a few thousand dollars annually to their budget. The risk exposure and coverage levels of the companies are the main factors affecting these amounts.

Q2. Does public liability insurance cover employee injuries?

Workers’ compensation insurance typically covers injuries to employees. Public liability insurance cannot cover the insured's employees.

Q3. Can sole traders get public liability insurance?

Definitely, a cover that shields sole traders from the occurrences of property damage or personal injury due to their business activities is the one they require.

Q4. How can I determine the amount of coverage my business needs?

You need to consider the potential danger elements in your business, check the acceptable insurance coverage in your line of business, and the cost of the claim. Consulting with insurance experts is essential to ensure you have the right cover for your business.

***This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

Small Business Public Liability Insurance: Everything You Need to Know

Small businesses venture on a journey full of both opportunities and risks. A company will always aim for growth and customer satisfaction. However, it is equally essential to ensure that the business is protected against unexpected claims. Public liability insurance for small businesses is among the most significant protective measures that any small business owner should consider.

Such a policy provides protection against legal fees, claims from third parties, and unexpected financial difficulties. In this blog, we will explore the components of public liability insurance, its importance for small businesses, and how to select the right policy for your specific insurance needs.

Key Takeaways

- Small business public liability insurance covers third-party injury and property damage.

- It includes compensation, defence costs, and related legal fees.

- Different from Professional Indemnity Insurance, it focuses on physical damage.

- Brokers and tailored insurance packages help small businesses get flexible cover.

What is Small Business Public Liability Insurance?

Small business public liability insurance covers your company if third parties make a complaint that they have suffered personal injury, property damage, or have received another type of loss due to your business operations.

To illustrate, if a customer falls on uneven flooring in your store and sustains an injury, your public liability insurance may provide coverage for their treatment costs, as well as any legal expenses incurred if they file a lawsuit.

No doubt, even the most careful business owners can be hit by accidents. This insurance protects you from having to pay massive compensation claims on your own.

Why Public Liability Cover is Essential

Though the safest method is always preferred, accidents are sometimes inevitable. The aftermath of an incident for small businesses can be so huge and suffocating that it may be hard for them to recover. It is therefore not surprising that public and products liability insurance is regarded as one of the most essential types of insurance.

Protects Against Third-Party Injury and Property Damage Claims

Accidents can occur in any location, even if a person is extremely cautious. If someone slips, falls, or the property is damaged, and these incidents are related to your work, then the responsibility lies with your company.

Covers Legal Costs and Defence Expenses

Legal proceedings can be costly, no doubt. A policy of public liability insurance covers the expenses of the lawyer who will defend a case. It also provides coverage when the issue is not with you.

Supports Business Stability

Public liability insurance is often required when dealing with local authorities, landlords, or contractors, though requirements may vary by industry and region. Public Liability cover can afford you financial security, but it also creates a good impression of you.

How it Differs from Other Insurance Products

Business owners are often confused about the differences between public liability insurance and other types of policies. Recognising these differences will help you avoid being overwhelmed by extra coverage or losing the protection of your rights.

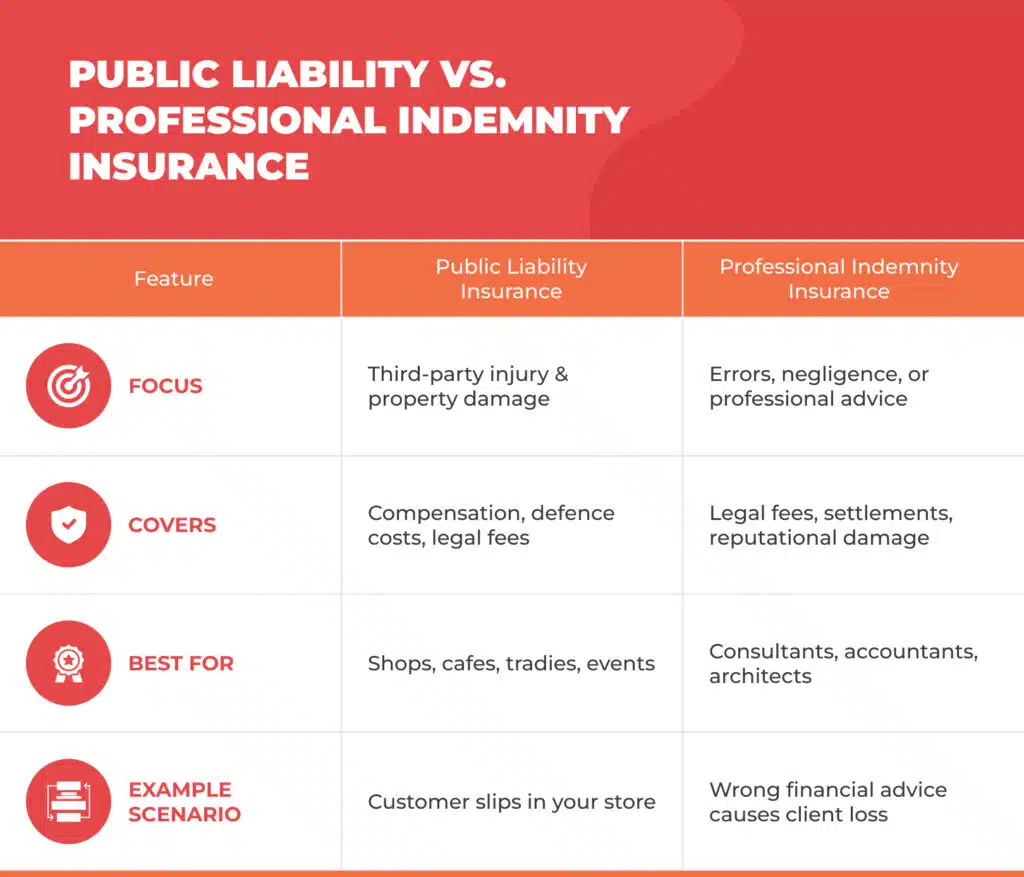

Public Liability vs Professional Indemnity Insurance

Public liability insurance covers only cases of physical injury and property damage directly caused to third parties. In contrast, professional indemnity insurance serves as a shield against financial losses resulting from the provision of professional advice, services, or negligence.

Consider a situation where a consultant gives incorrect advice. In this case, the consultant will then require an indemnity insurance policy. On the other hand, a café owner is required to have a public liability insurance policy to ensure the safety of customers.

Specialised Coverage for Premises and Negligent Activities

Public liability insurance typically includes coverage for events occurring at your location or resulting from your business's carelessness, which is often excluded from other types of insurance.

Product Liability and Recalls

Few auto insurance policies cover product liability resulting from claims due to a product that was sold or made by the insured that caused harm. This option is generally the most important one in the mentioned industries, such as food and electronics.

Key Features of Business Insurance Packages

A smaller business rarely requires just one policy. On the other hand, business insurance cover can be more effective when combined with other insurances that match their field of work, such as public liability insurance.

Types of Cover for Business Needs

- Sole traders typically pair public liability insurance with product liability insurance.

- Commercial car insurance is just the right solution for work vans, delivery trucks, and cars.

- Business premises insurance protects against the destruction of buildings.

For example, the hospitality sector might have packaged cover for food poisoning or injuries that occur during the administration of first aid.

Flexible Business Insurance Solutions

Insurers offer a range of cover options in terms of payments, policy details, and target audience identification. Not only can the cover be tailored to the client's specific requirements, but it can also be tailored to the client's particular compliance aspects and financial situations.

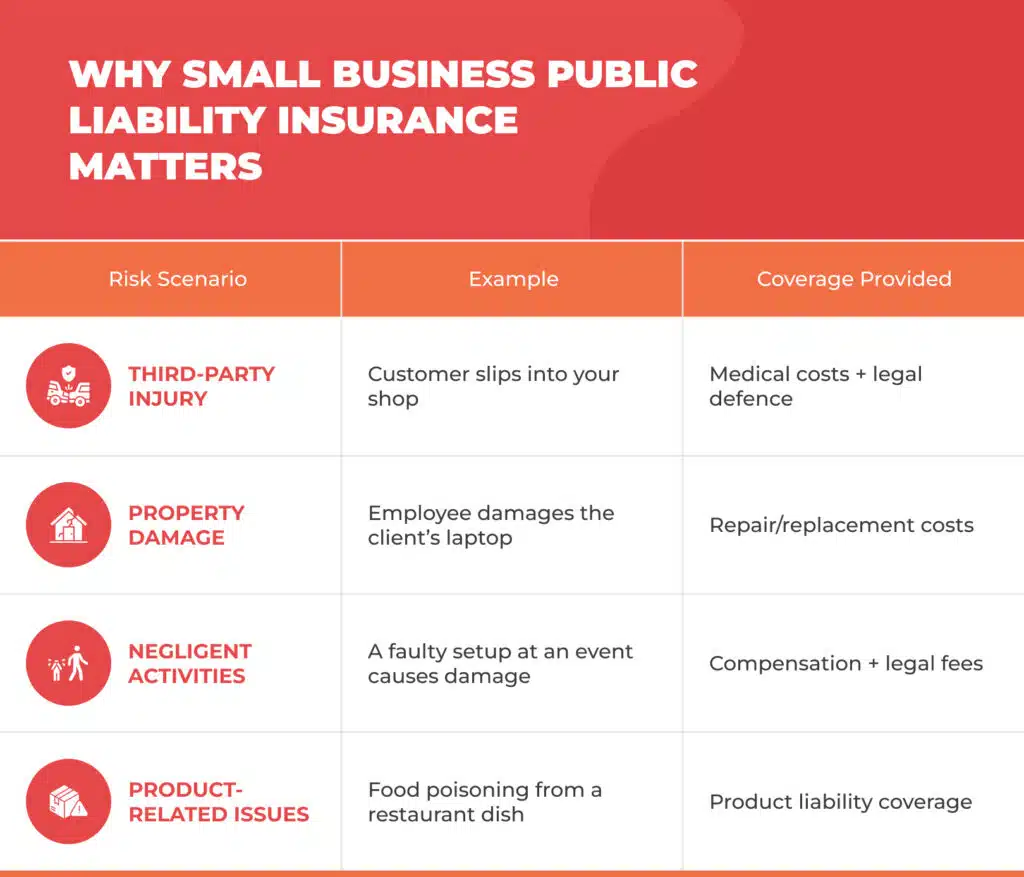

Common Public Liability Claims and Coverage

It is only after examining real-world instances that the significance of insurance sometimes becomes evident. Small businesses in various industries often face similar types of claims, and understanding these claims highlights the benefits of public liability insurance.

Examples of Typical Claims for Small Businesses

- Customer injuries on your premises: A shopper falls on a wet floor, a café customer is burned by spilled hot coffee, or a gym member trips over equipment.

- Damage to third-party property: A tradesperson destroys a client’s driveway by unloading the heavy equipment, or a contractor breaks a window during renovations.

- Negligent business activities: A defective product injures a consumer, or an employee’s careless performance leads to the injury or loss of a person outside the business.

Although these situations may appear minor, they have the potential to escalate into compensation claims of thousands of dollars quite rapidly.

Understanding Legal Fees and Defence Costs

It is surprisingly one of the small businesses for which the cost of a legal defence, even in a minor legal case, is a significant financial burden. Legal bills can grow large very quickly, and if you don't have insurance, they can be very costly. Small businesses often underestimate the number of legal processes they must follow.

- Coverage for Legal Liability: Public liability insurance provides coverage for lawyer fees, court costs, and settlements.

- Financial Loss Prevention: It eliminates the risk that your business may experience a cash flow issue due to the specified event.

- Extra Disbursements: Heavy industries may incur additional disbursements, such as safety investigations or regulatory penalties for non-compliance with safety standards.

How to Choose the Right Business Insurance Policy

Finding the right insurance policy for your business is more than just meeting the legal requirements. Such a business cover will guarantee your company's uninterrupted operation in times of unexpected events. The large number of insurance products has made it necessary for small business proprietors to perform a complete evaluation of what fits their businesses the best, including the potential risks and available amounts of money.

Factors to Consider for Your Business Type and Size

Every business must deal with unique types of risks that are specific to that particular business. A small café faces the risk of the disappearance of the coffee it sells. On the other hand, an IT consultancy has a completely different risk profile. A sole trader’s specific needs are entirely different from those of a multi-staffed company that is growing. When going through policies, it is essential to consider a number of factors, including:

- The type of business: Retail businesses most likely require product liability insurance, whereas more service-oriented companies may need professional indemnity insurance in addition to public liability.

- Business size: The potential risk increases with the number of customers, staff, or locations.

- Cover limits: Choose an amount of cover that represents the worst-case scenario your business can face. For instance, a tradesperson operating in residential homes might be allowed to have lower limits than a contractor working in big commercial spaces.

Working with a Business Insurance Broker

For instance, if you're unsure where to begin, a business insurance broker can simplify the process for you. Brokers assess your risks, compare policies from various companies, and recommend the most suitable solutions for you. Additionally, they can:

- Get an online quote that reflects the correct pricing for your insurance.

- Speak in simple terms about what is included in the cover.

- Ensure that you are fully covered and have your certificate of insurance ready for contracts or any other obligations.

The advice of a broker is highly beneficial for small businesses, especially when they are in a situation where they cannot afford to lack protection or pay an excessively high premium.

Protect Your Business with Public Liability Cover in 2025

The business environment will undoubtedly become increasingly complex in the future. Every year, rules become stricter, customers expect more, and new risks emerge. Public liability insurance must adapt to these changes.

Business owners of small businesses must ensure that their policies adequately cover the risks associated with their industry, possess the necessary policy documents, such as a certificate of currency, and comply with relevant insurance, tax, and legal requirements. This approach will equip your business to handle upcoming challenges better if adopted.

Not sure which cover best fits your small business? You can obtain tailored quotes from licensed insurance brokers such as VIM Cover and safeguard your business with public liability insurance. Get started today!

FAQs

Q1: Do all small businesses need public liability insurance?

Yes. A business of any size that has dealings with customers, suppliers, or the general public should have this cover.

Q2: How much cover for public liability do I require?

The level of cover is conditioned by your industry and the level of risk you are exposed to. The standard amount of coverage typically ranges from $5 million to $20 million.

Q3: Is public liability insurance a tax-deductible expense?

Yes. The payments for business insurance policies are typically deductible from the business's taxable income, classified as a business expense.

Q4: Do employees have protection under public liability?

No. Staff injury claims will be satisfied through the workers' compensation insurance scheme. Public liability is a safety net for the injured third party only.

This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

What Is Public Liability Insurance and Why Does It Matter in 2026?

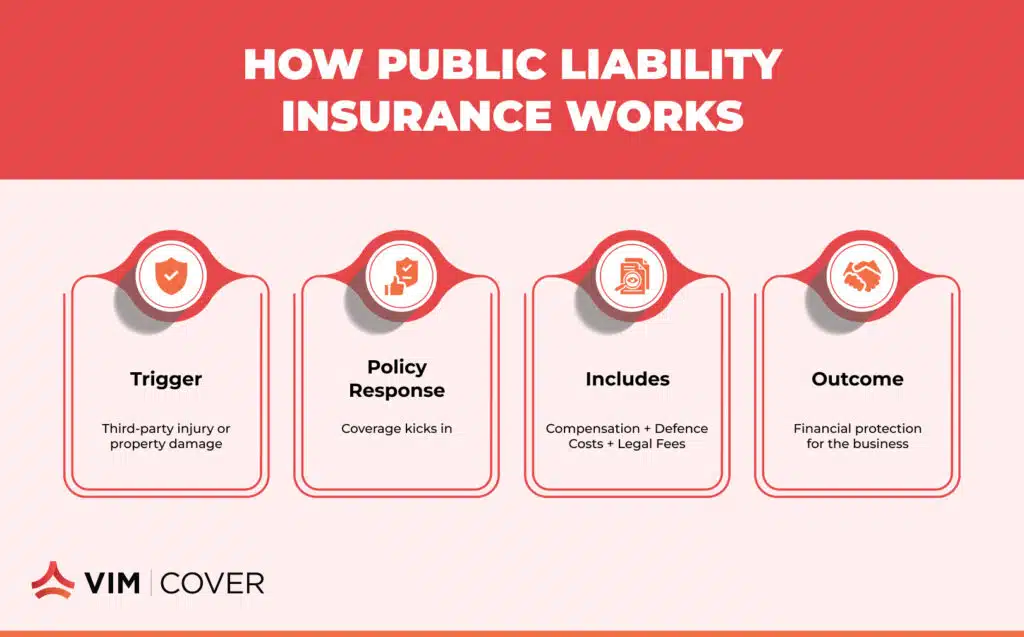

Public liability insurance aims to shield business owners from the ‘financial blows’ mentioned above. In 2026, with more stringent regulations in place and more willing customers regarding claims, such a policy is more than a nice-to-have. For many business owners, it is simply a matter of survival. Every business in Australia has to embrace growth and manage associated risks. It is always possible that something will go wrong, such as a customer slipping and falling on your foyer floor or a staff member accidentally damaging a client’s property. It is also possible that some products you sell might injure some customers. All these incidents can result in expensive litigation and compensation for the customer.

Key Takeaways:

- Public Liability Insurance helps businesses protect themselves from lawsuits and claims made by third parties for injury or damage to their property.

- It is a necessity for small businesses and professions, such as trades, hospitality, real estate, and beauty, which face customer risks and interaction daily.

- Every business should find the right policy by determining the business risks, coupled with coverage and other policies for added protection.

Understanding Public Liability Insurance

Public liability insurance covers any legal and compensation expenses arising from business activities that result in injury or property damage to third parties not involved in your business. The ‘third person’ can be a customer, a supplier, or even a bystander. Insurance brokers like VIM Cover specialise in providing essential coverage to protect your business from potential liabilities arising from third-party property damage or personal injury claims.

You can obtain quotes from licensed insurance brokers such as VIM Cove.

What Does Public Liability Insurance Cover?

- Third-party injury and property damage claims

If a person trips on a loose cable in your office or an employee scratches the client’s car while unloading the equipment, you will have to pay for the resulting expenses. These are specifically the expenses that Public Liability insurance covers. - Business activities leading to liability issues

Every industry carries risks. A carpenter might damage a wall while installing cabinets, or a beauty therapist might cause an allergic reaction during treatment. Cover ensures you don’t carry the full financial burden of these situations. - Risk exposure from products or services

A faulty product or service gone wrong can result in expensive claims. Even small businesses that think their risk is low can find themselves exposed when products reach the public.

How It Differs from Other Insurance Policies

- Comparison with indemnity insurance

Professional indemnity insurance covers mistakes and omissions in the advice and any other professional services rendered. More general in scope, public liability covers personal and property damages. - Relation to product liability and professional indemnity

Product liability often sits within public liability cover, while professional indemnity is sold separately. Together, they provide stronger protection. - Role in a comprehensive business insurance package

Many business owners bundle liability with other policies like workers' compensation, management liability, or cyber insurance. Public liability forms the backbone of these packages.

Why Business Owners Need Public Liability Insurance

Many business owners underestimate their exposure until it’s too late. A single claim can stretch into tens of thousands of dollars — a sum that can easily wipe out profits or, in extreme cases, shut a business down.

Who Should Consider This Coverage?

- Small business owners

Smaller operators rarely have the cash reserves to absorb large claims. Public liability cover provides security and allows them to operate with confidence. - Beauty professionals and real estate agents

Beauty services can lead to accidental injuries or skin reactions. Real estate agents frequently enter homes and run open inspections, exposing them to property damage claims. - Food-related businesses

Cafés, restaurants, and caterers carry a high risk when it comes to food poisoning or contamination. One claim can damage not just finances, but reputation as well.

Protecting Your Business Type and Activities

- Business premises and operations coverage

Liability cover protects you from incidents occurring at your premises or during everyday business operations. - Addressing unique business needs

Coverage can be tailored. A trades business might need higher limits than a freelance consultant, while event organisers may require additional protections. - Reducing property damage claims and liability risks

When a client’s laptop is damaged in an accident as minor as spilling a cup of coffee, a claim is immediately submitted. Having public liability insurance avoids these small vulnerabilities from turning into heavy losses.

How to Choose the Right Public Liability Insurance Policy

Not all insurance policies offer the same type of coverage. Business owners need to balance the coverage offered by the policy with the actual threats they face to obtain adequate protection. An insurance broker can help tailor a policy to your business needs.

Key Factors to Evaluate

- Understanding policy wording and coverage limits

Some policies offer exclusion clauses, while others have a variety of coverage limits. These clauses, along with the limits, have to be examined thoroughly to avoid unpleasant surprises at the time of a claim. - Assessing your business type and risk exposure

High-risk industries need higher coverage. A sole trader might get by with lower limits, but construction companies need more comprehensive protection. - Customising an insurance package

Public liability insurance can often be purchased along with other types of business insurance, tailoring your policy to fit the scope of your actual business activities.

Bundling Public Liability with Other Insurance Policies

- Including workers' compensation insurance

Essential for businesses with employees and often paired with liability cover for simplicity. - Adding product liability or cyber insurance

Product liability protects against defective goods, while your business may be subject to product liability claims, and cyber insurance addresses the widening scope of cyber attacks. Insurance addresses the growing threat of online attacks. - Considering management liability insurance

Protects directors and officers, complementing public liability cover. - Exploring income protection or life insurance

These personal covers give business owners and families an added layer of security.

Regional Considerations for Public Liability Insurance

Insurance obligations differ across states and territories, so business owners must ensure their policy complies locally.

Requirements Across Australia

- Australian Capital Territory

In the ACT, some industries must show proof of liability insurance before obtaining licences or permits. - Northern Territory

In the NT, stricter requirements often apply to the construction and hospitality sectors. - State-specific business insurance policies

Make sure your insurance covers all local regulations in the states of Queensland, Victoria and Western Australia.

Working with Trusted Providers

- Choosing an AAI Limited-backed policy

Providers with strong backing offer confidence that claims will be handled fairly. - Ensuring adequate insurance coverage

Businesses should review their policies regularly to keep pace with growth and new risks. - Protecting against liability claims and property damage

Reliable providers reduce stress, ensuring claims don’t derail business operations.

Maximising the Benefits of Public Liability Insurance

Public liability insurance enables businesses to operate without fear. It’s more than just an insurance policy; it’s an asset that empowers businesses to expand and take on new projects with confidence, ensuring compliance and peace of mind.

- Safeguard your business operations and premises.

Now that your policy is set up, you can focus on serving your clients selflessly without the fear of claims. - Minimise risks with a tailored business insurance package

Bundling other policies with liability cover helps ensure your protection is both complete and economical.

Frequently Asked Questions

- Public liability insurance for sole traders: is it a legal requirement in Australia?

Although it may not be a legal requirement for every business, coverage proof is often a precondition for commencing operations in many sectors, for several local government bodies, and for customers. - Public liability insurance cost: how much does it cost to be insured?

Most of the time, it is determined by the specific industry, the risks involved, and the coverage limits. A small consultancy will pay several hundred dollars in coverage, while firms in the construction or hospitality sectors will expect higher premiums. You can obtain quotes from licensed insurance brokers such as VIM Cover. - Public liability and professional indemnity insurance: what is the distinction?

Public liability covers third-party injury and property damage, whereas indemnity insurance is taken out to cover claims arising from negligence, error, or poor professional advice.

Public liability insurance is often required when dealing with local authorities, landlords, or contractors, though requirements may vary by industry and region.

What Does Public Liability Insurance Cover?

Key Takeaways

- Pubic liability insurance is intended to safeguard businesses from claims made by third parties for bodily injuries or damages to property caused by business activities.

- This is particularly important for self-employed professionals, small business proprietors, and individuals working in public environments, visiting clients, or having customers come to their location.

- Alongside compensation and the legal and claims investigation expenses, the policy cover excludes injuries to employees, poor quality, and cyber risks from coverage.

- Your line of work and contracts determine the cover amount needed, and the insurance may differ based on the business.

- Working with business insurance specialists helps you choose the right level of cover and avoid gaps.

- Insurance brokers like VIM Cover in Australia meet real-world business needs and contractual obligations with specially designed cover options.

Understanding Public Liability Insurance Coverage

What is Public Liability Insurance?

Every business, regardless of size, may be exposed to physical and financial harm to a third party. Public Liability Insurance protects the business against claims of personal injuries or property damages, which otherwise leaves the business to incur huge compensation expenses, along with the costly legal fees.

Picture a customer slipping in your shop in Sydney or a tradie accidentally damaging a client's property while working on-site in Melbourne. Without cover, you could be personally responsible for the cost of the claim. With a proper insurance policy, those expenses are managed for you.

VIM Cover offers policies designed for Australian businesses, so whether a small business owner running a café in Brisbane or operates as a contractor in Perth, your cover reflects the specific risks you face.

Who Needs Public Liability Insurance?

In Australia, a considerable number of small to medium-scale enterprises hold public liability insurance as a business requirement drafted by the landlords, councils, or contractors. The sole traders, freelancers, and small business operators who interact with customers directly are more susceptible to these risks.

It's essential for:

- Businesses operating in shopping centres or local markets.

- Trades working on construction job sites.

- Home office professionals who welcome clients to their property.

- Beauty professionals provide personal services to customers.

In some industries, proof of a Public Liability policy is a condition of getting work. Having cover in place shows you take responsibility for the safety of your customers and the wider public.

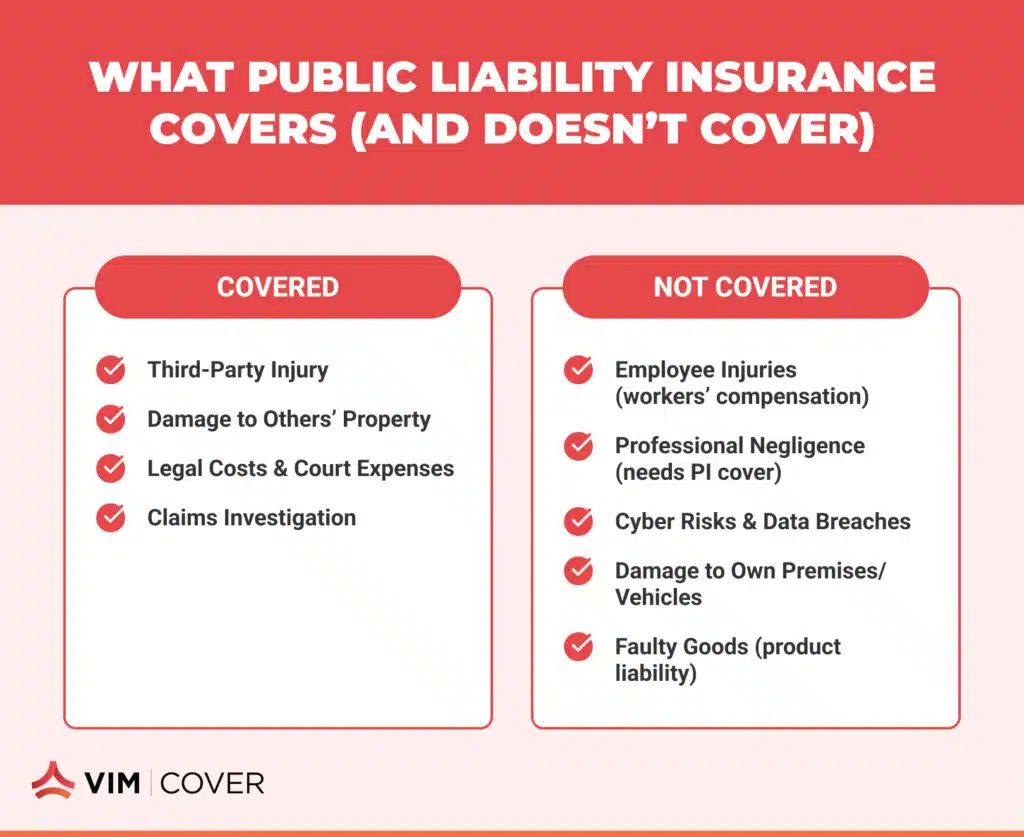

What Does Public Liability Insurance Cover?

Public liability insurance explained simply: it protects you if your work or premises cause harm to other people or their property.

Typical cover includes:

- Compensation for third-party injury.

- Repair or replacement costs for damaged business premises or personal belongings that don't belong to you.

- Legal action and the associated legal costs if a claim is taken to court.

Imagine a client who trips over an extension cord in your Adelaide office or who, in a meeting in Hobart, pours hot coffee on a customer’s lap. In both cases, public liability insurance may pay for these expenses. VIM Cover assists Australian businesses to tailor their Public Liability Insurance Cover to their specific needs, thereby eliminating the issues of overinsurance and gaps in cover.

What Isn't Covered by Public Liability Insurance?

Public liability insurance doesn't cover every type of risk. Some matters fall under different policies:

- Errors in advice or work that are dealt with through Professional Indemnity Insurance.

- Injuries to staff that require workers' compensation insurance under Australian law.

- Contractual liability or machinery breakdown.

- Cybercrime or data breaches, which need cyber insurance.

- Damage to your own business premises or motor vehicles.

- Faulty goods that require product liability insurance.

Exclusions are particularly relevant when it comes to Australia, given that different rules or insurance obligations may exist in its various states and territories. VIM Cover defines what is and isn't covered so that additional policies or protections can be arranged if necessary.

Choosing the Right Public Liability Policy for Your Business

Factors That Influence Policy Coverage

Required levels of cover may vary depending on the work, location, and any applicable contractual obligations. For instance, a council in New South Wales may mandate a certain minimum public liability insurance for market stallholders, whereas a landlord in Victoria may have different criteria.

Other factors include:

- The nature of your work and the potential liabilities involved.

- The policy wording and full details of what's covered.

- Your budget and cash flow.

- Any specific legal requirements in your industry?

Taking the time to compare options ensures you meet obligations without paying for unnecessary extras.

Why Seek Help From Business Insurance Specialists?

The last thing you would like to see is a policy misunderstanding during a claim. When it comes to business insurance specialists, they will guide you on what is appropriate for your financial situation. They clarify definitions, revealing the nuances, and see the value in additions like income protection or contents cover.

VIM Cover provides this guidance for Australian businesses, making sure your Public Liability policy fits your industry and keeps you compliant with local requirements.

How to File a Public Liability Insurance Claim

Steps to Ensure a Successful Claim

If you need to make a Public Liability claim in Australia, these steps can help:

- Record the incident immediately with photos, witness names, and medical or repair reports.

- Notify your insurer promptly for direction on what to do next.

- Submit all required documents, including your Public Liability Insurance cover details.

- Cooperate with investigations and keep communication clear and timely.

- Check your policy wording to confirm the incident is covered.

Common Challenges During Claims

Claims can take longer to resolve if documents are not filled out, or when the Public Liability Insurance Applied is not clear for the specific case. Also, disputes regarding contractual liability and disputes regarding cover limits are the most common issues.

Working with a responsive insurance broker like VIM Cover helps you navigate these hurdles. The clearer your policy is at the start, the smoother the claims process will be.

Key Insights on Public Liability Insurance

As for Australian businesses, Public Liability Insurance is a requirement. It offers protection from claims that emerge from ordinary interactions, including legal costs, compensation, and business disruption, which are costly.

Every business, even if it's a sole trader working at a local market or a developing business owning multiple sites, utilises Public Liability policies. With a reputable Australian insurance broker such as VIM Cover, you are able to attain both peace of mind and protection, letting you concentrate on your work and knowing that any unforeseen circumstances are covered.

FAQs About Public Liability Insurance

- Is public liability insurance mandatory in Australia?

Public liability insurance is not required by law for all businesses; however, several industries, landlords, and councils do make it part of their operating conditions. For instance, at some markets and on some construction sites, stallholders and contractors are required to obtain proof of insurance before they start work.

- How much public liability insurance do I need?

The business, the contract, and the evaluation of risk determine the correct value of insurance coverage. Some businesses only need a couple of million dollars of coverage, while others might need upwards of $20 million. Always make it a point to review the contracts and have a conversation with an insurance advisor to determine the most appropriate coverage.

- Does public liability insurance cover employees?

Public Liability Insurance does not cover employees. Injuries of employees are taken care of under workers' compensation insurance, which is compulsory in Australia. Public liability insurance only takes care of third parties, such as customers and guests.

- What’s the difference between public liability and professional indemnity insurance?

Public liability covers the injury or damage to the property of other people as a result of an accident. Professional indemnity covers financial losses resulting from advice given, services provided, or mistakes made, as well as losses of meritorious work. It is beneficial for many businesses to hold both types of insurance.

- How do I claim public liability insurance?

Insurers need to be notified as soon as possible. Alongside the notice, supporting documents need to be sent as well, which can include photographs, medical documents, and invoices related to the repairs. The claim has a better chance of getting approved if you collaborate with the insurance company regarding the needed documents and information for their investigation.

**This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

Comprehensive Food Truck Insurance for 2026

Discover unparalleled protection for your food truck insurance needs with VIM Cover’s comprehensive food truck insurance policies. Designed for Australian truck owners, our policies ensure affordability and reliability, keeping you secure on every journey. We offer a rapid quote for approved applicants. Please fill out the form below to receive a fast quote.

Key Takeaways on Food Truck Insurance

- Food trucks face double exposure: road accidents + customer liability.

- A single food poisoning claim can cost thousands in legal fees.

- Equipment breakdowns or food spoilage can stop operations overnight.

- Tailored insurance helps protect cash flow and keeps you compliant.

- VIM Cover offers customised policies with fast claims support.

Food trucks face risks beyond the kitchen. A road accident can damage your vehicle and equipment, spoiled stock can wipe out profits, and legal fees can be incurred in cases of food poisoning or other allergies. Unlike restaurants, food trucks are exposed to both road mishaps and other safety liabilities. These uncertainties make it essential to have a more business-focused and personalised insurance, which allows you to run your business with minimal worry. The right cover not only protects your cash flow and keeps you compliant but also ensures your mobile business stays open after an unexpected setback.

Why Food Truck Insurance is Crucial for Your Business?

Unlike a fixed restaurant, your food truck is both your motor vehicle and your business premises, meaning you carry double the exposure on the road and in service. That's why the right food truck insurance isn't optional; it's essential. Also, it's equally important to have the right type of insurance that matches your business and its running.

For operators, it’s worth noting that insurers in Australia must meet regulatory standards set by APRA (Australian Prudential Regulation Authority), ensuring you’re dealing with a licensed and compliant provider. This gives food truck owners confidence that their policy is backed by a regulated and trustworthy insurance company.

Unique Risks Food Trucks Face

It includes:

- Accidental damage - This includes vehicle damage, such as a minor prang, or even if a vehicle is written off, including accidental damage to cooking equipment, which prevents any immediate service.

- Food poisoning & personal injury – Costly legal claims can arise due to foodborne illness or a slip near your service window.

- Food spoilage & equipment breakdown – If your fridge fails overnight or your generator cuts out at a festival, spoiled stock is money lost.

- Legal liability – Every public interaction, from parking in crowded areas to serving hot food, exposes you to potential compensation claims.

- Optional covers – Extra protection, such as cash flow cover, can keep bills paid if downtime stops you from trading.

How Insurance Protects Operators?

Let's understand some of the standard insurances:

- Personal accident & workers' compensation covers truck owners and their staff in case of mishaps, which include burns, cuts, or other injuries sustained while at work.

- Medical expenses & legal costs – In case a customer sues over injury or illness, your business insurance policy can handle the hospital bills and lawyer fees.

- Insurance claim support – A good provider ensures that claims for insured events, such as theft, breakdowns, or accidents, are processed quickly, thereby reducing downtime.

- Peace of mind for operators – With cover in place, food truck owners can focus on what matters most: serving customers and growing the mobile business without the constant worry of "what if."

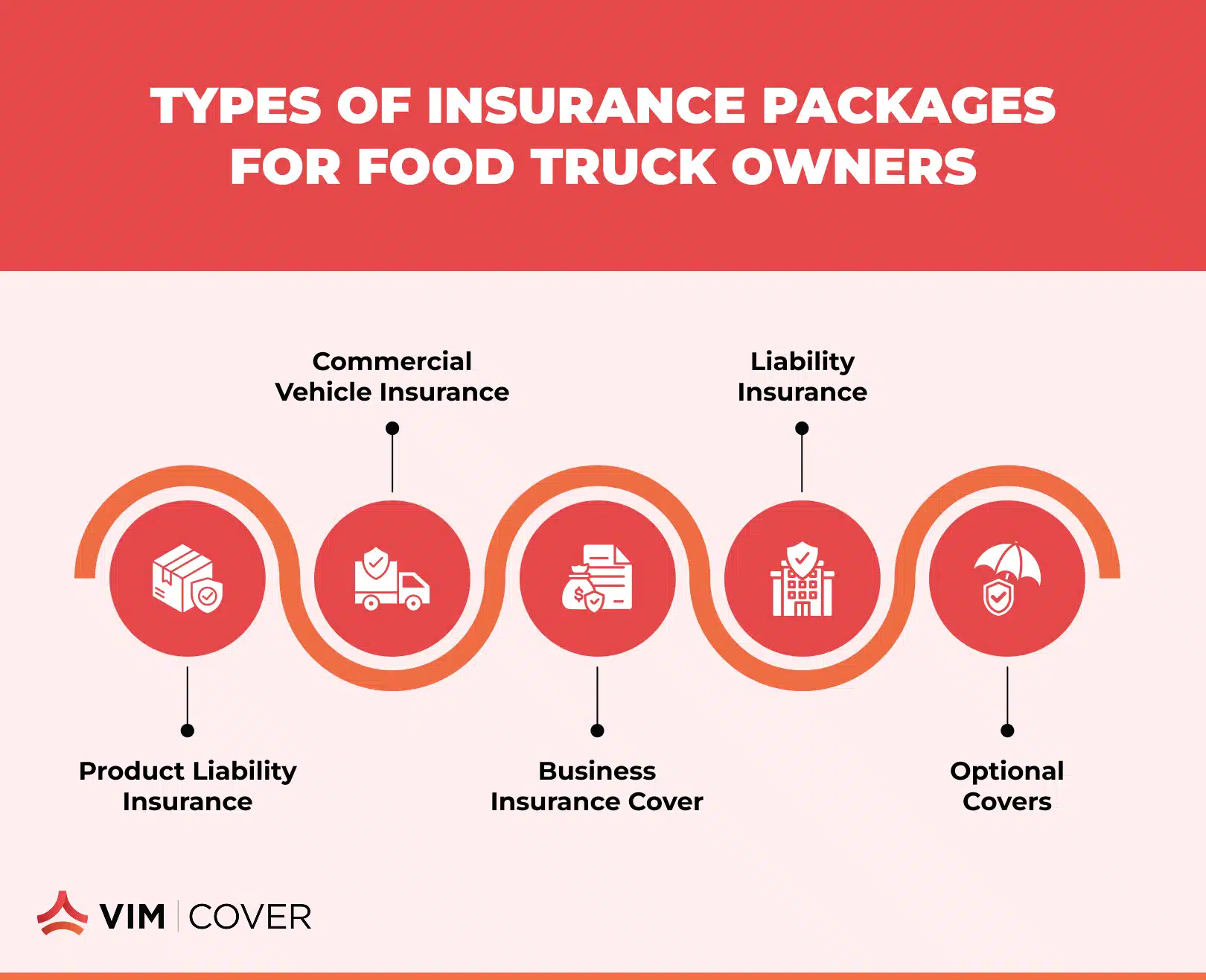

Types of Insurance Packages for Food Truck Owners

Product liability insurance protects against claims of:

- food poisoning

- allergic reactions

- Covering legal fees and compensation.

Commercial vehicle insurance covers:

- the truck itself,

- repairs after accidental damage,

- fit-out and cooking equipment inside.

Business insurance cover extends to:

- stock, cash

- portable equipment

- losses from theft, fire, or food spoilage.

Liability insurance protects against:

- Legal costs if a customer or third party suffers personal injury

- Property damage during the course of business activities.

Optional covers, such as equipment breakdown or downtime protection, help:

- stabilise income when generators fail

- fridges stop working

- You are unable to operate due to an insured event.

It's advisable to read and understand policy wordings and Product Disclosure Statements before signing up for any particular insurance cover to avoid claim issues.

How VIM Cover Provides Superior Insurance Solutions?

We understand that no two mobile food trucks are alike and have specific business needs. Irrespective of whether you run a coffee van, a gourmet burger truck, or a multi-vehicle fleet, customisable insurance packages allow you to pick and choose the level of accidental loss you would like to cover. We offer a rapid quote for approved applicants. Please fill out the form below to receive a fast quote.

Unlike one-size-fits-all insurance providers, we work through experienced insurance brokers who focus on understanding your day-to-day risks. Based on your business operations, we suggest that you opt for comprehensive cover that extends to business premises, staff, and broader business activities. Our flexible cover options let you choose the best for your business.

What sets us apart from many insurance companies is our fast and transparent claims process. Food truck operators don't have time for paperwork delays; their streamlined approach ensures you're back on the road as quickly as possible. The policy terms are written to reflect the realities of mobile businesses, avoiding unnecessary coverage and reducing higher premiums that other providers often charge.

Protect Your Mobile Food Business with the Right Coverage

A tailored business insurance quote from VIM Cover ensures you only pay for what truly matters — no unnecessary extras, just the right cover for the risks your food truck faces daily. Policies are designed around your actual operations, whether you run a coffee van with portable generators, a gourmet burger truck with high-value cooking equipment, or a fleet serving significant events.

Coverage can extend to:

- Breakdowns & spoilage – protection when fridges, freezers, or generators fail.

- Liability claims – cover for food poisoning, personal injury, or property damage caused during service.

- Business interruption – income support when an insured event forces you to stop trading.

By securing a plan built for your business model, you safeguard cash flow, meet legal liability requirements, and keep your mobile business operational with minimal disruption. Protection is not just compliance; it's a guarantee that you can stay on the road and serve customers with peace of mind.

FAQs About Food Truck Insurance with VIM Cover

- Does food truck insurance cover both the vehicle and kitchen equipment?

Yes. With VIM Cover, policies can bundle commercial vehicle insurance with coverage for cooking equipment, refrigeration, and fit-outs, ensuring your entire mobile setup is protected under one plan.

- What happens if food spoilage occurs due to a power failure?

Food spoilage caused by equipment breakdown or power outages can be included in your policy. VIM Cover helps you recover costs so your cash flow isn't disrupted.

- Can I insure multiple food trucks under one policy?

Absolutely. VIM Cover offers fleet policies for operators with multiple trucks, making it easier and often more affordable to manage insurance for your mobile business.

- How does VIM Cover handle claims for food poisoning incidents?

If a customer files a claim for food poisoning or personal injury, your liability coverage will take effect. VIM Cover ensures a transparent and fast claims process, minimising downtime and legal costs.

- Are there flexible insurance options if I only operate seasonally?

Yes. VIM Cover can tailor cover options for seasonal food truck operators, so you're only paying for the protection you need when your business is active.

**This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

Comprehensive Commercial Truck Insurance Guide for 2026

Key Takeaways about Commercial Truck Insurance

- Protects business vehicles and drivers from major risks.

- Covers accidents, liability, downtime, and natural disasters.

- Flexible options: comprehensive, third-party, and add-ons.

- Extra cover: life, property, transit, and roadside support.

- VIM Cover delivers fast quotes and tailored solutions.

Running trucks for business isn’t simple. Breakdowns, accidents, and even weather events can affect businesses and their operations, often causing delays in deliveries and other regular activities. It also leads to a lot of back-and-forth to get things on track. That’s why having commercial truck insurance is more than just meeting a requirement on paper; it’s about protecting your people, your trucks, and your cash flow.

At VIM Cover, we work with businesses across Australia to make sure they’re not left exposed. The right cover means fewer worries and a faster recovery when things don’t go as planned.

Why Commercial Truck Insurance Matters?

Protecting Business Operations

If your trucks are on the road for business purposes, you’re carrying risk every kilometre. Good cover ensures:

- Business vehicles are protected if damaged or written off.

- Truck drivers and owner-operators can work with peace of mind.

- Major risks like accidental damage, public liability, or third-party property damage don’t turn into major financial losses.

Key Benefits of the Right Coverage

A firm insurance policy does more than replace a damaged truck. It helps your business stay steady when unexpected costs hit.

- Financial protection – Keeps your cash flow intact when repair or replacement bills arrive.

- Risk coverage – From natural disasters to accidents involving dangerous goods.

- Downtime cover – Helps with income loss if a truck is off the road.

- Business continuity – Support during claims so your operations don’t stall.

Types of Commercial Insurance for Trucking Businesses

Core Options

- Comprehensive or complete insurance – Covers physical damage, accidental damage, and total loss.

- Third Party Property Damage – Protects against damage claims from others.

- Roadside assistance – Reduces costly delays if a truck breaks down.

- Prime mover cover – Designed for high-value vehicles critical to freight.

Add-Ons and Extras

Depending on your setup, you may also need:

- Life insurance for owner-operators.

- Property insurance for depots or warehouses.

- Marine cargo insurance if your transport extends offshore.

- Custom options based on carrying capacity and mixed personal use.

How to Choose the Right Commercial Truck Insurance Policy for Your Business Needs

Step 1: Match Commercial Truck Insurance Cover to Your Business Activities

Think about:

- The risks in your line of work (long-haul, dangerous goods, interstate freight).

- What’s already included in your policy documents?

- Your driving history and financial situation both affect premiums.

Step 2: Pick a Reliable Insurance Provider

Not all insurance companies cover the requirements of truck insurance. Before you decide:

- Compare truck insurance quotes across providers.

- Look for insurers with experience in transport and strong claims support.

- Ask for clear Target Market Determination (TMD) documents to ensure the policy is designed for businesses like yours.

How Commercial Truck Insurance Protects Your Business

Comprehensive Risk Management Solutions

The right commercial truck insurance is a key component of innovative risk management. It:

- Shields you from compensation claims and third-party liability.

- Covers accidental damage or total loss.

- Keeps operations running with superior claims service and access to replacements.

- Provides tailored solutions so you don’t pay for cover you don’t need.

Compliance and Business Continuity

Insurance is about protection while your trucks are on the go, as well as staying compliant with state laws and avoiding unwanted losses. Policies that meet Target Market Determination guidelines and address specific business needs help keep you aligned with state regulations. This reduces legal risks while ensuring your trucks have the right insurance cover.

Why Partner with VIM Cover? Your Right Commercial Truck Insurance Partner

We specialize in policies that work for real businesses, not cookie-cutter solutions, and our insurance covers ensure adequate liability coverage for your trucks tailored to their specific needs. We help you:

- Find cover that fits your business use and vehicle types.

- Add extras like downtime cover or roadside assistance when needed.

- Get a truck insurance quote in just 60 minutes for eligible applicants. That means in case of emergencies, when you require the right coverage or comprehensive insurance for your truck, we are here to assist you.

- Rely on a team that supports you through the claims process.

Many business owners also wonder, Are business vehicles more expensive to insure? The answer depends on factors such as vehicle type, usage, and risk profile, which can significantly impact insurance costs.

We offer customised commercial truck insurance policies, flexible cover options, and, for approved applicants, a fast 60-minute quote service to keep your business moving without downtime.

FAQs – Commercial Truck Insurance with VIM Cover

Q: How quickly can I get a truck insurance quote with VIM Cover?

We know time matters in business. That’s why VIM Cover offers a rapid turnaround on most truck insurance quotes, so you’re not stuck waiting.

Q: Does VIM Cover provide cover for dangerous goods?

Yes. Our policies can be tailored for the transportation of dangerous goods, ensuring you stay protected while meeting compliance requirements.

Q: Can I insure a mixed fleet under one policy?

Absolutely. Whether you run prime movers, delivery vans, or light trucks, we can customise cover for a wide range of vehicle types and carrying capacities under a single policy.

Q: What if my truck breaks down or is off the road?

We offer downtime coverage and roadside assistance options, helping to reduce income loss and keep your business operations steady during unexpected repairs.

Q: Does VIM Cover only provide truck insurance?

No. Alongside comprehensive truck insurance, we also offer a range of additional products, including business insurance, property insurance, public liability insurance, and transit insurance, to provide you with complete protection for your business and personal needs.

Q: Why choose VIM Cover over other insurance providers?

Unlike generic insurance companies, we focus on the trucking industry. That means tailored advice for the type of insurance based on your requirements, flexible extras, fast quotes, and hands-on customer support during the claims process.

**This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

Comprehensive Light Truck Insurance Guide for 2026

At VIM Cover, we understand that every light truck operator has different needs, whether you’re moving goods across town, running a fleet of goods-carrying vehicles, or transporting dangerous goods. That’s why we offer customised light truck insurance policies, flexible cover options, and, for approved applicants, a fast 60-minute quote service to keep your business moving without downtime.

Key Takeaways:

- Light truck insurance is essential for goods-carrying vehicles up to 4.5 tonnes GVM, protecting against theft, damage, liability, and downtime losses.

- VIM Cover offers customised policies with optional add-ons like downtime cover, transit insurance, and dangerous goods protection.

- The right policy offers peace of mind with vehicle coverage, theft protection, accident liability, and business continuity support.

- Understanding your vehicle type, cargo value, and business operations is key to selecting the right level of coverage.

- VIM Cover’s 60-minute quote service ensures fast, tailored insurance solutions for businesses of all sizes.

- Bundling your truck insurance with life, travel, or home insurance can enhance your protection strategy.

- Opting for a provider like VIM Cover, known for transparency and strong support, can improve your claims experience.

What Is Light Truck Insurance?

Light truck insurance is designed for goods-carrying vehicles with a specific carrying capacity, which is often up to 4.5 tonnes GVM and can be personalised for business use or personal purposes. It protects you from accidental damage, theft, property damage to other people’s property, and even total loss of your vehicle.

For businesses, this type of cover isn’t just a compliance tick; it’s a safeguard that keeps business vehicles on the road and earning a stable income (in case of any mishap), even after an insured event.

Understanding Light Trucks and Insurance Needs

Light trucks are versatile workhorses (as they call it) that range from delivery vans to small tippers, and their insurance needs vary from heavy commercial trucks. Policies are built to reflect:

- The carrying capacity and type of vehicle.

- Frequency and nature of business activities.

- Whether they carry dangerous goods, operate as mobile plant, or are used for mixed personal and business purposes.

An effective truck insurance policy ensures you’re covered for real-world risks, not just what’s written on paper.

Key Features of Light Truck Insurance

A strong, comprehensive truck insurance policy can include:

- Comprehensive cover for your vehicle and your property.

- Theft cover and accidental loss protection.

- Downtime cover to support your cash flow while your truck is off the road.

- Compensation claims for personal injury or damage caused to others.

The level of cover you choose will determine how well you’re protected when it matters most.

Why Businesses Need Light Truck Insurance?

Supporting Business Vehicles and Operations

For transport operators and owners of goods-carrying vehicles, light truck insurance is more than a formality. It’s essential for keeping operations running, especially when dealing with dangerous goods or time-sensitive and/or perishable goods delivery.

During an insured event, having the right cover can help with repair costs, replacements, and even provide a temporary hire vehicle to keep jobs moving.

Small Business Insurance Benefits

Many insurers offer small business insurance packages that combine comprehensive coverage for trucks with other insurance products. These can be customised for:

- Specialised freight

- Mobile plant transport

- High-value goods

- Multi-vehicle fleets

It’s not just about protection, it’s about peace of mind for owners and employees.

Choosing the Right Light Truck Insurance Policy

Factors to Consider

Before selecting a truck insurance policy, weigh your:

- Type of vehicle and carrying capacity.

- Driving history and risk profile.

- Level of cover, including downtime cover and comprehensive coverage.

- Specific clauses in the Policy Wording and relevant Product Disclosure Statement.

Working with Insurance Brokers and Providers

An experienced insurance broker can help you clearly understand the aspects of the insurance, cut through the jargon, compare cover options, and match you with an insurance provider that fits your financial situation and specific needs. Choose providers with a clear Target Market Determination and responsive customer support to guide you through the claims process.

Additional Insurance Products to Consider

For businesses looking to protect more than just their trucks, pairing your commercial motor cover with other insurance products can strengthen your safety net:

- Home insurance – To protect personal property from damage or theft.

- Travel Insurance – For business or personal trips involving valuable goods.

- Boat Insurance – For commercial or personal watercraft.

- Life Insurance – Ensures financial stability for your family or business partners if the unexpected happens.

- Transit insurance – Covers goods in transit from pickup to delivery.

Ready to protect your business?

Get a customised VIM Cover light truck insurance quote in under *60 minutes. Speak to our team today for personalised cover recommendations.

Protecting Your Business with the Right Cover

The right policy cushions your business from costly disruptions and keeps operations running smoothly. It’s about matching insurance to the real risks you face, not paying for what you don’t need.

- Downtime cover to offset income loss during repairs

- Protection for high-value or sensitive cargo

- Add-ons for dangerous goods and mobile plant

- Policy terms that fit your vehicle type and workload

Learn more about how to get a truck insurance quote in 2026.

Why Choose VIM Cover for Light Truck Insurance?

When it comes to protecting your business vehicles, you need more than just a standard policy; you need a partner who understands the risks and challenges you face every day.

VIM Cover offers:

- Comprehensive truck insurance for a wide range of vehicle types and carrying capacities.

- Flexible extras like downtime cover, transit insurance, and customised policy wording for your specific needs.

- A proactive and responsive customer support.

- Our 60-minute turnaround for quotes for qualifying applicants.

Schedule an appointment with us today!

FAQs – Light Truck Insurance

Q: Can I get a light truck insurance quote quickly with VIM Cover?

Yes. In certain circumstances, VIM Cover offers a 60-minute rapid quote service so you can get insured without delays.

Q: Does VIM Cover offer cover for dangerous goods or mobile plant vehicles?

Absolutely. Our truck insurance policies can be tailored for dangerous goods, mobile plant, and other specialised uses.

Q: What makes VIM Cover different from other insurance providers?

We combine comprehensive coverage with personal service, flexible policy design, and fast turnaround times, all while ensuring your specific needs are met.

Q: Can I bundle my light truck insurance with other products at VIM Cover?

Yes. You can combine your truck cover with options like home insurance, travel insurance, or life insurance to protect more of what matters to you.

**This article provides general information only and does not take into account your specific circumstances. You should seek advice from a licensed insurance professional before making decisions.

How to Get a Truck Insurance Quote in 2026?

Key Takeaways:

- What’s included in a truck insurance quote (and what’s not).

- The difference between Comprehensive cover, Third Party Property Damage, and other policy types.

- How factors such as vehicle type, cargo, and business use affect your price.

- Add-ons like downtime cover and transit insurance can save you when things go wrong.

- How to compare insurance providers and read the fine print before you sign.

- What to expect during the claims process and how to avoid delays.

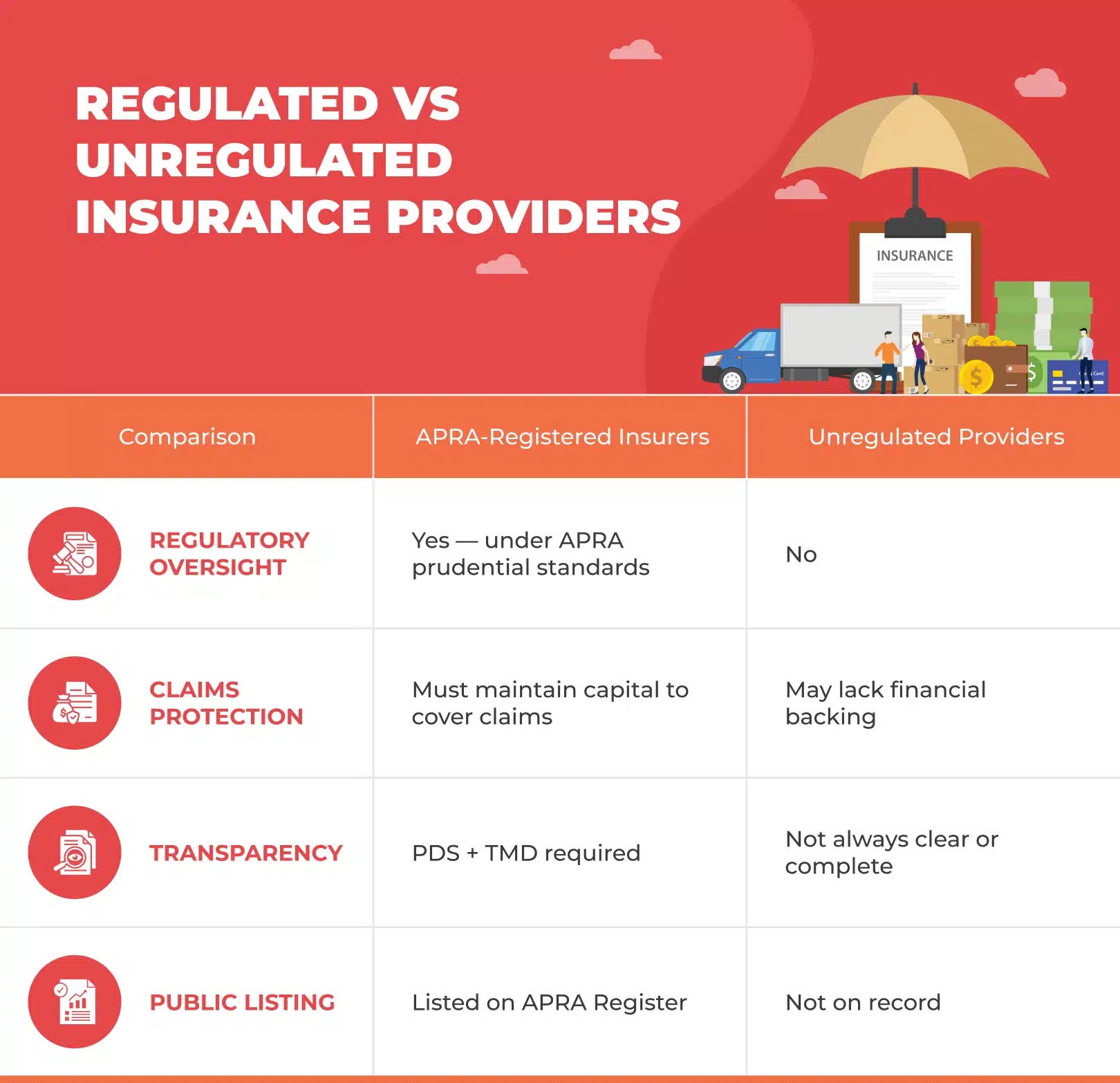

If you own a truck or manage a fleet, insurance isn’t optional; it’s essential. In 2026, getting a truck insurance quote is more than just filling out forms. Insurers assess what you drive, how you use it, and your claims history before offering cover. And you can compare offers only from APRA‑authorised insurance companies to make sure your provider meets national standards.

Want a Quote in 60 Minutes?

If you’re short on time, we offer a 60-minute rapid quote turnaround for eligible businesses. That means less waiting, more peace of mind, and faster protection for your truck or fleet.

Get your truck insurance quote in under 60 minutes here!

What is Included in a Truck Insurance Quote?

Most insurance companies include several critical components in your quote. Review the Insurance Council of Australia guidelines to understand industry best practices for commercial motor insurance, including how risks like property damage and liability are handled.

Most insurance companies will include the following in your truck insurance quote:

1. Type of Cover

You’ll typically choose from a few key policy types:

- Comprehensive cover – Covers your truck for theft, accidental damage, vandalism, and property damage to others, even if the accident was your fault.

- Third Party Property Damage – Protects you if your vehicle causes damage to someone else’s vehicle or property, but not your own.

- Third Party Fire and Theft – A balance between cost and protection, covers others' property, plus fire or theft damage to your vehicle.

You may also consider Public Liability Insurance, Compulsory Third Party (CTP), or Third Party Insurance, depending on your operations and state requirements.

2. Business Use and Specific Activities

Your quote reflects how and where you operate:

- Local, regional, or national transport

- Dangerous goods, refrigerated goods, or mobile plant operations

- Business-related storage or depot details

Your business use directly affects pricing and eligibility.

3. Vehicle Information

Insurers evaluate:

- Truck make, model, age

- Carrying capacity

- Whether you operate light trucks, rigid trucks, or prime movers

- Modifications like mobile cranes, tail lifts, or onboard computers

Accurate info ensures a valid quote and helps avoid policy disputes.

4. Driving & Claims History

Your driving history, past claims history, and even your financial situation play a role in determining premium levels and excess options.

Operators with strong safety records often access lower premiums or better coverage limits.

5. Optional Benefits and Add-On

Coverage options like Transit Insurance or Downtime Cover are standardised across the Australian insurance market. Understanding typical definitions and claims processes is easier when referring to the Insurance Council of Australia’s guidance.

6. Policy Inclusions, Costs, and Documentation

Every quote includes:

- A detailed premium (monthly or annually)

- Breakdown of inclusions and exclusions

- Every quote should point you to a Product Disclosure Statement and a Target Market Determination, as insurers must follow APRA’s prudential standards for general insurers regarding transparency and governance.

- A clear Target Market Determination

- Your rights to general and personal insurance advice

Understanding your policy wording and the full scope of your cover is essential before committing.

Understanding Truck Insurance Coverage

A truck insurance quote typically includes one or more of the following cover types:

Comprehensive Cover

Covers your truck for accidental damage, theft, fire, and property damage to others. It’s ideal if your truck is essential to your income or is of high value.

Third Party Property Damage & Public Liability

Essential if your truck damages someone else’s vehicle or property. Public liability insurance covers incidents involving injury or damage during loading, unloading, or delivery.

Add-Ons That Matter

Depending on your business, you can include:

- Downtime cover – income protection if your truck is off the road

- Transit insurance – protects your cargo during transport

- Windscreen, hire vehicle, and legal liability extras

Each policy can be customised to fit your business, from a single light truck to a fleet of prime movers.

Additional Insurance Types You May Need

Your truck insurance quote may cover the vehicle, but running a business often involves other risks. Depending on your operations, you might also need:

Travel Insurance for business-related trips

If you or your team regularly travel for work, whether interstate or regional, Travel Insurance can cover unexpected costs like trip cancellations, delays, or personal injury.

Boat Insurance for companies with marine operations

For transport companies that also operate near ports or on water, Boat Insurance protects vessels used for loading, delivery, or marine transport. It’s especially relevant for businesses involved in intermodal freight.

Life Insurance to protect business owners and employees

If you’re a business owner or employ drivers, Life Insurance adds a layer of security for families and teams. It helps protect income, manage business debts, or support succession planning, a valuable asset for small business operators.

Why Truck Insurance Protects Your Business Operations?

Things go wrong. Accidents happen. Trucks break down. A good truck insurance policy makes sure you’re not paying for it all out of pocket.

What the Right Policy Covers

- Covers repair costs and property damage

- Takes care of legal liability if you're at fault

- Downtime cover helps you manage lost income

- Gives owner-drivers and transport operators real peace of mind

What Kind of Vehicles Are Covered?

- Light trucks, rigid trucks, and prime movers

- Work trucks, vans, and business cars under Commercial Vehicle Insurance

- Trucks carrying dangerous goods or fitted with mobile plant

It’s all about keeping your trucks on the road and your business moving.

Factors That Impact Truck Insurance Cost

No two quotes are the same. Your truck insurance cost depends on a few key details that insurers use to assess your risk.

What Insurers Look At?

- Your driving and claims history, and your financial situation.

- The truck’s carrying capacity and how it's used for business activities

- The type of insurance you’re after, Comprehensive cover, Third Party Property Damage, or something in between

- Your financial situation, including the ability to absorb risk

Whether you’re an owner-driver or managing a fleet, these factors shape your premium.

Understanding the Fine Print

Before signing anything:

- Read the Product Disclosure Statement (PDS) for the full details

- Make sure the policy matches your business: check the Target Market Determination (TMD)

- Look into optional benefits that could improve your cover (and increase the cost)

Precise policy wording helps avoid headaches later, especially at claims time.

How to Find the Best Truck Insurance Providers?

With so many insurance companies out there, finding the right fit comes down to knowing what to look for and asking the right questions. You can read our comprehensive guide about Light Truck Insurance for 2026 here.

Steps to Get the Right Coverage

- Always choose insurers listed on APRA’s official register of authorised general insurers. This guarantees they are monitored for financial stability and regulatory compliance.

- Be ready with your personal information, vehicle details, and business needs

- Speak to an authorised representative who can give clear, tailored advice, not just a sales pitch

Insurance Options Beyond Truck Insurance

Depending on your setup, you might need:

- Fleet insurance for multiple trucks or vehicles

- Home Insurance or Landlord Insurance to protect business-related properties

- Home Buildings coverage for owner-operators running from home

Get cover that fits your life, not just your truck.

Tips for Navigating the Truck Insurance Claims Process

Accidents happen. When they do, understanding the claims process can save you time, stress, and money.

What to Expect During Claims?

- For events like accidental loss, total loss, or property damage, your insurer will walk you through the required steps.

- You may need to submit documents, evidence, or repair quotes, stay organised.

- Liability claims and compensation claims can take longer, especially if third parties are involved.

Many insurers now offer a streamlined process online, and some (like VIM Cover) even assign a dedicated claims team to support you.

Importance of General Advice and Customer Support

- Reliable Customer Support can make or break your experience, especially during stressful situations.

- Seek general advice before committing to a policy or during a claim if you're unsure of your next step.

- Go with a provider that offers a wide range of insurance solutions, so you’re not left uncovered when it matters most.

It’s not just about getting your truck fixed. It’s about getting back on the road with confidence.

Types of Trucks Covered Under Commercial Vehicle Insurance

Whether you're hauling freight across states or running tools between worksites, your policy should match your vehicle type.

Here's what most commercial truck insurance policies can cover:

- Light trucks – often used by tradies, couriers, and small business owners

- Rigid trucks – ideal for local deliveries, moving services, or specialist freight

- Prime movers – used for long-haul freight, heavy haulage, and intermodal operations

- Mobile plant & mobile cranes – often used in construction and industrial settings

- Vehicles carrying dangerous goods require more tailored risk assessments

A quality Truck Insurance Policy should reflect how your vehicles are used for business purposes and the risks they face day-to-day.

Transit Insurance: Do You Need It?

If your trucks are carrying cargo, Transit Insurance can be a game-changer.

It covers accidental damage, theft, or loss of goods while in transit, which is especially crucial for freight companies and owner-drivers transporting high-value cargo or working with fragile or perishable items.

You can also extend this cover to include:

- Natural disasters (flood, fire, storm)

- Theft while parked overnight

- Third-party Fire and Theft for high-risk routes

Is Fleet Insurance Better for Growing Businesses?

Running more than a few vehicles? Fleet Insurance can often provide:

- Bulk discounts across all registered vehicles

- Easier renewals with one policy, not ten

- Streamlined claims and admin

Fleet cover is ideal for transport operators, logistics businesses, and companies with business vehicle insurance needs across multiple locations or drivers.

Even small businesses with just three or four trucks can often access entry-level fleet solutions.

Do You Need Life Insurance as a Truck Operator?

It might not be the first thing on your mind, but if you're an owner-driver, business partner, or running a transport company, Life Insurance matters.

- It protects your family or business if something happens to you

- Can be bundled with other products (like Travel Insurance and Boat Insurance) if your operations involve different risk areas

Many insurance providers now offer business-focused life cover with flexible options based on your risk level and financial situation.

Secure the Right Truck Insurance Quote for Your Business